Good Saturday morning to all of you here on r/StockMarket. I hope everyone on this sub made out pretty nicely in the market this past week, and are ready for the new holiday-shortened trading week ahead.

Here is everything you need to know to get you ready for the trading week beginning December 20th, 2021.

Market turbulence may be a theme in the holiday week as investors fret over omicron, the Fed - (Source)

Stocks could be volatile in the coming week, with thin volume exaggerating moves in both directions ahead of the Christmas holiday.

The market was whipsawed in the past week, with the Nasdaq down about 2.9% since Monday and lagging the other major averages on a weekly basis. Technology stocks were at the center of major market swings, as investors reacted to the spreading omicron Covid variant and the Federal Reserve's hawkish shift.

"As we head into the last two weeks of the year, we know volume is light and volatility can also pick up," said Jeff Kleintop, chief global investment strategist at Charles Schwab. "There's the possibility of a Santa rally, but there's also the possibility that the lack of volume can lead to dramatic swings to the downside as well."

While December is typically positive for stocks, the traditional Santa Claus rally is the historically positive market performance that often comes in the last five trading days of the year and first two of January, according to Stock Trader's Almanac. As the saying goes, if Santa doesn't call, bears may come to Broad and Wall — the street address of the New York Stock Exchange.

A thinner market near the end of the year

So far, the S&P 500 is still up 1.2% for December, but it's down nearly 1.9% for the week. The broad-market index has a roughly 23% gain for the year. The index ended Friday at 4,620.

"The Santa Claus rally this year is a little tough to call because the market has done so well up to this point. Building on that momentum is a bold call," said Michael Arone, chief investment strategist at State Street Global Advisors. "Volumes are going to decrease, and that's likely to lead to greater volatility into year end. It wouldn't surprise me if markets close the year strongly, but with the omicron variant and the Fed tightening, it just seems anxiety is at high levels."

Strategists haven't given up on the idea of a late December to early January rally. However, with the selling pressure, it could be more difficult for the seasonal year-end buyers to boost the market. The thinness of the market may also make it tricky to gauge how stocks will trade into January.

"I think it's going to be hard to get a real tell on the market — the light volume and the fact there's going to be relatively little economic news or corporate news. It's going to be just incremental news on omicron," said Kleintop.

He said earnings in the past year have been a catalyst for stocks, with companies beating estimates and raising guidance. That could turn the tide in the next earnings season in mid-January, if stocks continue to move lower.

"This time we might get a lot of dividend increases. There's a lot of cash out there," he said. Kleintop said expectations are for just an 8% gain in corporate profits in 2022, and that could move higher since companies appear to be managing margins better than expected.

In the week ahead, there are several economic releases to watch. The markets will be most fixated on personal consumption expenditures next Thursday, as the so-called PCE deflator is the inflation data most watched by the Federal Reserve. The report follows November's hot consumer price index, which was up 6.8% on a year-over-year basis.

Arone said the market will also monitor the consumer confidence index release next Wednesday for inflation expectations. The University of Michigan's consumer sentiment index is out Thursday.

Key real estate indicators are also out next week, with existing home sales on Wednesday and new home sales Thursday. Durable goods are also out Thursday.

The market is closed for the Christmas holiday on Friday.

Bond market confusion

As stocks gyrated, bond yields went down in the past week, especially after the Fed announced Dec. 15 that it would speed up the end of its bond-buying. The central bank also provided a new interest rate forecast which showed members expect as many as three hikes next year, when previously they did not forecast any.

The Fed also removed the description of inflation as "transitory" from its statement.

Bond yields move opposite price, so the move lower in rates was surprising to market professionals. It would be logical to have expected a jump in yields at the shorter end of the market, which is most influenced by Fed policy. For instance, the 2-year Treasury yield was at 0.63% Friday afternoon, below the 0.67% level it was at ahead of the Fed news.

The benchmark 10-year yield was at 1.44% before the Fed's announcement. It had fallen to 1.37% by Friday morning and was at around 1.40% in afternoon trading.

Yields initially inched higher Friday afternoon after Fed Governor Christopher Waller said the central bank could raise interest rates as early as March. Goldman Sachs economists had been expecting a March hike, but most expected the Fed to wait until May or June because it will end its bond program in March.

"I do think the omicron scare has got people spooked. On the long end, it's weighing on it," said Wells Fargo's Michael Schumacher. "The front end doesn't make a lot of sense. We just heard from the Fed... The front end should really be taking its marching orders from Powell."

China easing?

While the Fed and the Bank of England have recently moved to tighten policy, another economic superpower may be doing the opposite.

Schumacher and Kleintop said a positive surprise for markets could come from China ahead of Monday's trading.

"On Monday, we'll all be watching China with what they do with their loan prime rate. There's a chance they could cut it," Kleintop said.

"If China is going to re-inflate their economy, that would be a real boost to global growth," he said.

What to do

Kleintop said investors should stay fully invested. He noted that because of the big rotations in market leadership this year, investors should be more diversified.

"Every time we started to see a breakout with value, it was crushed with another virus outbreak. We should be seeing growth stocks outperform here, as cases rise, but they haven't made a new high relative to value since the news of omicron," said Kleintop.

Kleintop noted that the tech sector is highly valued, with its price-earnings ratios 10 points above the 20-year average. The forward price-earnings for global tech was 28.5 Friday. He said that compares to the global energy sector, trading on a 12-month forward price-earnings ratio of 9.5, about nine points below its average.

"This is the widest gap we've seen between the growthiest of the growth and the value sectors," Kleintop said. "We haven't seen tech make a new high relative to energy since before omicron. Certainly, there's the Fed weighing on valuations as well as there's the idea there's going to be less liquidity pouring into these favorite stocks."

Kleintop said he does not see a big gain for the market in 2022, like this year, and investors should look abroad for some better gains.

"We see a positive year for equities but nothing like this year," he said. "There's a potential outperformance by Europe and international next year, after they underperformed."

This past week saw the following moves in the S&P:

S&P Sectors for this past week:

Major Indices for this past week:

Major Futures Markets as of Friday's close:

Economic Calendar for the Week Ahead:

Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:

S&P Sectors for the Past Week:

Major Indices Pullback/Correction Levels as of Friday's close:

Major Indices Rally Levels as of Friday's close:

Most Anticipated Earnings Releases for this week:

Here are the upcoming IPO's for this week:

Friday's Stock Analyst Upgrades & Downgrades:

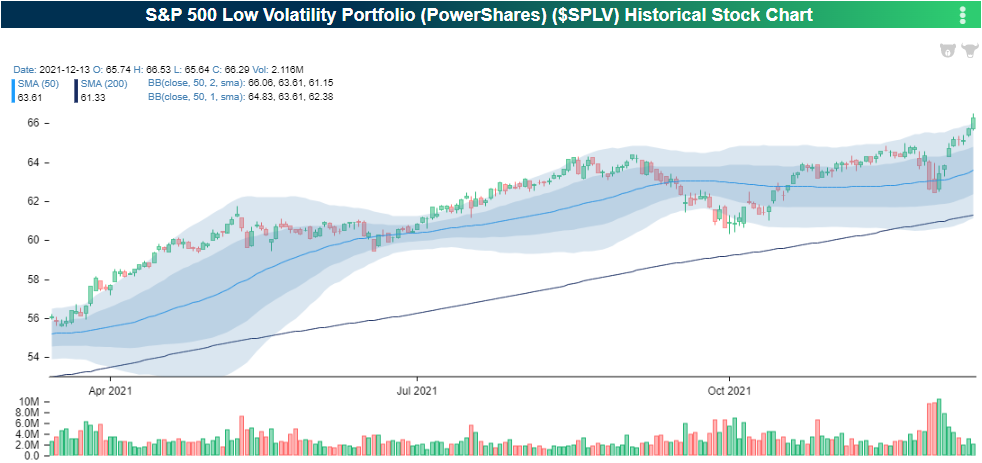

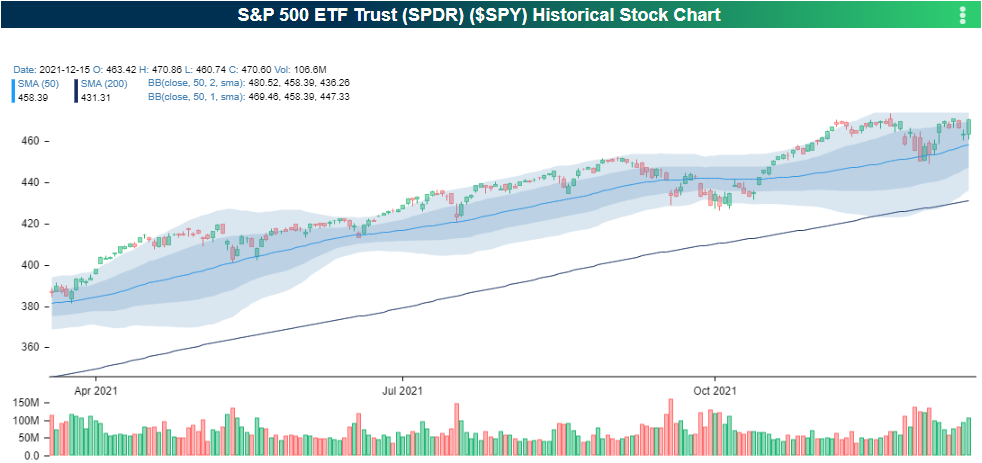

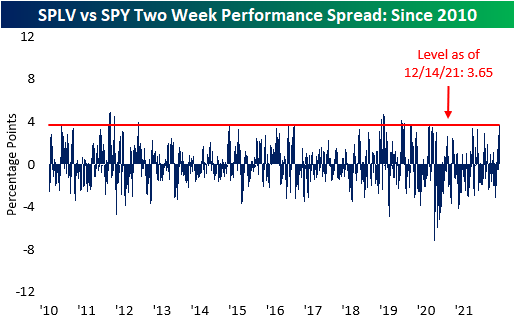

Outperformance from Low Volatility

Over the last two weeks, low volatility names have outperformed the broader market. The PowerShares S&P 500 Low Volatility ETF (SPLV) has ticked 6.83% higher over the last 10 trading days as of yesterday's close. During the same time period, the SPDR S&P 500 ETF (SPY) moved 4.36% higher. Investors have poured into safer names so far in December, but SPLV has still underperformed SPY on a YTD basis. Over the last three months, the performance of these two ETF's has been essentially identical with SPLV breaking out to all-time highs, while SPY struggles to break out. Although investors are not necessarily selling off equities broadly, they are gaining exposure to lower volatility names, which could be interpreted as taking a more conservative posture.

The two-week performance spread between SPLV and SPY is currently at an elevated level, and as of earlier this week (12/14) was at its widest level since 1/31/20, which is less than a month before the COVID correction began. Investors should watch the performance of low volatility names moving forward, as continued outperformance would signal that investors are becoming increasingly risk averse.

Five Important Charts To See Right Now

As we head into the end of 2021, here are five charts that caught our attention.

First up, last week was one of the best weeks of the year for stocks, and that could be a good sign. "It turns out that big weeks like last week usually have the bulls smiling," explained LPL Financial Chief Market Strategist Ryan Detrick. "23 out of the past 25 times the S&P 500 Index gained at least 3.8% in a week, it was higher three months later."

As shown in the LPL Chart of the Day, the S&P 500 closed up more than 3.8% in a week on 25 occasions since March 2009, with last week being number 26. As you can see, the future returns 1-, 2-, and 3-months out are extremely strong.

Second, we are nearing the second half of December, which historically is when stocks tend to do well during this usually bullish month. In fact, returns actually get better if the S&P 500 is negative in November (check) and up more than 20% heading into the final month of the year (check).

Third, the second year of the Presidential Cycle tends to be the worst of the four-year cycle and it is up the least often as well. Although we expect stocks to still do well in 2022, this is a reminder it likely won't be another run-away bull market like we saw in 2021.

Breaking this down by new Presidents versus re-elected Presidents and it is quite clear that year 2 under a new President historically has been quite weak. Then again, this said year 1 shouldn't be very good and that sure hasn't been the case this year.

Lastly, breaking things down by quarters, it becomes very clear the next three quarters are some of the worst of the four-year cycle, before a very strong fourth quarter.

Mid-December Low Buy Point

December typically starts out weak. And it has. But despite the recent worrisome headlines about the Fed, inflation and Omicron stocks typically begin the yearend rally right here around mid-month. As you can see here in the chart while this year has clearly exhibited more volatility, stocks have tracked the usual December seasonal pattern of weakness in early December. So with market seasonality reasserting itself these past few months the prospects look good for the rally to resume.

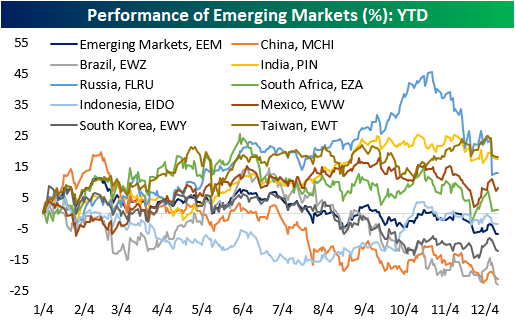

Pockets of Strength in Emerging Markets

So far this year, the US has outperformed every other country on the planet. Broadly speaking, developed economies have outperformed emerging economies. The iShares MSCI Emerging Markets ETF (EEM) has declined 6.8% in 2021, but this does not necessarily mean that performance across every emerging economy has been negative. Although China, Brazil, and South Korea have been particularly weak (three of the top six countries of exposure for EEM), countries like Taiwan, India, Russia, Mexico, and South Africa have experienced positive returns this year.

Just like individual sectors in the US cannot be expected to perform equally, emerging economies don't always perform in unison with each other. Differences include natural resources, political & legal structure, trading partners, and much more. Although EEM has declined on a YTD basis, the average performance of the nine countries that we tracked was a modest loss of 0.1%, and the spread between the best performer (Taiwan) and the worst (Brazil) is currently 41.3 percentage points. Moving forward, investors may want to consider selecting individual countries to gain emerging market exposure, as the broader ETFs tend to have a large concentration in just a few countries. Emerging markets are inherently higher-risk investments in comparison to developed nations due to uncertainty in future prospects, but in the long run, there are excellent opportunities within pockets of emerging markets, although not all countries will see the same performance.

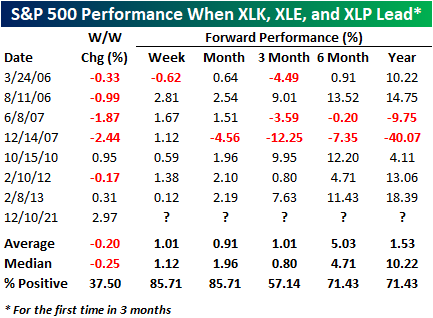

Strange Bedfellows: Technology, Energy, and Consumer Staples Lead

Technology (XLK), Energy (XLE), and Consumer Staples (XLP) tend to trade quite differently from each other for a variety of reasons. The Consumer Staples sector tends to be more defensive in nature as spending on the 'essentials' tends to hold up better in times of uncertainty than spending on more cyclical goods. XLE is largely levered to the price of energy commodities but also acts as an inflation hedge. Technology, meanwhile, tends to do best in a bullish tape as investors gravitate towards sectors with the brightest growth prospects. Because these sectors have different exposures, it is uncommon to see weeks like last week where these three sectors top the leaderboard for a given week. In fact, this has only occurred 9 times since the start of 2000, and two of those occurrences were in back-to-back weeks at the end of 2007.

In the table below, we show each of the prior weeks that Technology (XLK), Energy (XLE), and Consumer Staples (XLP) were the three top-performing sectors (without a prior occurrence in the last three months) along with the S&P 500's performance over the last following week, month, three months, six months, and one year. In more than half of the prior eight occurrences, the equity market was lower during weeks when this occurred, and in the two prior weeks where the S&P 500 was higher, it was up less than 1%. In other words, there has never been a week like the last one where the S&P 500 was up close to 3% and these three sectors topped the leaderboard. After the eight prior occurrences, the S&P 500 was consistently higher one week and one month later with positive returns six out of seven times. Moving further out, though, the consistency of positive returns was less. In fact, three months later, the S&P 500 was only higher four out of seven times, while six and twelve months later it was higher five out of seven times.

Somewhat ominously, the worst forward returns came after the occurrence almost exactly fourteen years ago in December 2007 when the S&P 500 went on to decline 40% in the following year. One difference between that period and last week, though, was that instead of those three sectors leading the market in a week where the S&P 500 was up over 2%, in that week the S&P 500 was down over 2%.

STOCK MARKET VIDEO: Stock Market Analysis Video for Week Ending December 17th, 2021

STOCK MARKET VIDEO: ShadowTrader Video Weekly 12.19.21

([CLICK HERE FOR THE YOUTUBE VIDEO!]())

(VIDEO NOT YET POSTED.)

Here are the most notable companies (tickers) reporting earnings in this upcoming trading week ahead-

- ($MU $NKE $CCL $BB $RAD $KMX $GIS $PAYX $BLDE $CTAS $FDS $MSM $EPAC $CVGW $APOG $CGNT $BLIN $CAMP $AIR $AVO $RFIL $YTRA $BRZE)

Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

Monday 12.20.21 Before Market Open:

Monday 12.20.21 After Market Close:

Tuesday 12.21.21 Before Market Open:

Tuesday 12.21.21 After Market Close:

Wednesday 12.22.21 Before Market Open:

Wednesday 12.22.21 After Market Close:

Thursday 12.23.21 Before Market Open:

([CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE.)

Thursday 12.23.21 After Market Close:

([CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE.)

Friday 12.24.21 Before Market Open:

([CLICK HERE FOR FRIDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK!]())

(NONE. U.S. MARKETS CLOSED IN OBSERVANCE OF CHRISTMAS DAY.)

Friday 12.24.21 After Market Close:

([CLICK HERE FOR FRIDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE. U.S. MARKETS CLOSED IN OBSERVANCE OF CHRISTMAS DAY.)

Micron Technology, Inc. $83.00

Micron Technology, Inc. (MU) is confirmed to report earnings at approximately 4:00 PM ET on Monday, December 20, 2021. The consensus earnings estimate is $2.01 per share on revenue of $7.66 billion and the Earnings Whisper ® number is $2.16 per share. Investor sentiment going into the company's earnings release has 73% expecting an earnings beat The company's guidance was for earnings of $2.00 to $2.10 per share. Consensus estimates are for year-over-year earnings growth of 145.12% with revenue increasing by 32.69%. Short interest has decreased by 11.8% since the company's last earnings release while the stock has drifted higher by 16.6% from its open following the earnings release to be 4.4% above its 200 day moving average of $79.48. On Friday, December 17, 2021 there was some notable buying of 4,882 contracts of the $77.00 put expiring on Thursday, December 23, 2021. Option traders are pricing in a 4.6% move on earnings and the stock has averaged a 4.5% move in recent quarters.

Nike Inc $161.36

Nike Inc (NKE) is confirmed to report earnings at approximately 4:15 PM ET on Monday, December 20, 2021. The consensus earnings estimate is $0.63 per share on revenue of $11.25 billion and the Earnings Whisper ® number is $0.72 per share. Investor sentiment going into the company's earnings release has 63% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 19.23% with revenue increasing by 0.06%. Short interest has decreased by 4.5% since the company's last earnings release while the stock has drifted higher by 6.8% from its open following the earnings release to be 6.4% above its 200 day moving average of $151.70. Overall earnings estimates have been revised lower since the company's last earnings release. On Monday, December 6, 2021 there was some notable buying of 10,743 contracts of the $185.00 call expiring on Friday, January 21, 2022. Option traders are pricing in a 4.7% move on earnings and the stock has averaged a 7.8% move in recent quarters.

Carnival Corp. $18.28

Carnival Corp. (CCL) is confirmed to report earnings before the market opens on Monday, December 20, 2021. The consensus estimate is for a loss of $1.45 per share on revenue of $1.34 billion and the Earnings Whisper ® number is ($1.55) per share. Investor sentiment going into the company's earnings release has 42% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 28.22% with revenue increasing by 3,841.18%. Short interest has increased by 16.8% since the company's last earnings release while the stock has drifted lower by 28.1% from its open following the earnings release to be 27.0% below its 200 day moving average of $25.03. Overall earnings estimates have been revised lower since the company's last earnings release. On Tuesday, December 7, 2021 there was some notable buying of 7,512 contracts of the $25.00 put expiring on Friday, September 16, 2022. Option traders are pricing in a 7.9% move on earnings and the stock has averaged a 2.8% move in recent quarters.

BlackBerry Limited $9.17

BlackBerry Limited (BB) is confirmed to report earnings at approximately 5:05 PM ET on Tuesday, December 21, 2021. The consensus estimate is for a loss of $0.08 per share on revenue of $177.25 million and the Earnings Whisper ® number is ($0.08) per share. Investor sentiment going into the company's earnings release has 58% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 300.00% with revenue decreasing by 18.69%. Short interest has decreased by 1.6% since the company's last earnings release while the stock has drifted lower by 10.1% from its open following the earnings release to be 13.6% below its 200 day moving average of $10.62. Overall earnings estimates have been revised higher since the company's last earnings release. On Friday, December 17, 2021 there was some notable buying of 3,360 contracts of the $9.50 call and 3,236 contracts of the $8.50 put expiring on Thursday, December 23, 2021. Option traders are pricing in a 8.0% move on earnings and the stock has averaged a 7.2% move in recent quarters.

Rite Aid Corp. $12.05

Rite Aid Corp. (RAD) is confirmed to report earnings at approximately 7:00 AM ET on Tuesday, December 21, 2021. The consensus estimate is for a loss of $0.18 per share on revenue of $6.32 billion. Investor sentiment going into the company's earnings release has 75% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 145.00% with revenue increasing by 3.32%. Short interest has increased by 30.3% since the company's last earnings release while the stock has drifted lower by 14.1% from its open following the earnings release to be 32.3% below its 200 day moving average of $17.80. Overall earnings estimates have been unchanged since the company's last earnings release. On Thursday, December 9, 2021 there was some notable buying of 672 contracts of the $3.00 put expiring on Thursday, April 14, 2022. Option traders are pricing in a 10.5% move on earnings and the stock has averaged a 15.0% move in recent quarters.

CarMax, Inc. $137.54

CarMax, Inc. (KMX) is confirmed to report earnings at approximately 6:50 AM ET on Wednesday, December 22, 2021. The consensus earnings estimate is $1.49 per share on revenue of $7.34 billion and the Earnings Whisper ® number is $1.57 per share. Investor sentiment going into the company's earnings release has 48% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 4.93% with revenue increasing by 41.56%. Short interest has decreased by 6.7% since the company's last earnings release while the stock has drifted higher by 3.3% from its open following the earnings release to be 4.2% above its 200 day moving average of $131.96. Overall earnings estimates have been revised higher since the company's last earnings release. On Wednesday, December 8, 2021 there was some notable buying of 1,972 contracts of the $140.00 put expiring on Thursday, December 23, 2021. Option traders are pricing in a 4.4% move on earnings and the stock has averaged a 8.6% move in recent quarters.

General Mills, Inc. $67.65

General Mills, Inc. (GIS) is confirmed to report earnings at approximately 7:00 AM ET on Tuesday, December 21, 2021. The consensus earnings estimate is $1.06 per share on revenue of $4.82 billion and the Earnings Whisper ® number is $1.08 per share. Investor sentiment going into the company's earnings release has 67% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 0.00% with revenue increasing by 2.13%. Short interest has decreased by 27.9% since the company's last earnings release while the stock has drifted higher by 13.1% from its open following the earnings release to be 11.2% above its 200 day moving average of $60.83. Overall earnings estimates have been revised higher since the company's last earnings release. On Thursday, December 16, 2021 there was some notable buying of 3,028 contracts of the $72.50 call expiring on Friday, January 21, 2022. Option traders are pricing in a 5.5% move on earnings and the stock has averaged a 2.1% move in recent quarters.

Paychex, Inc. $123.89

Paychex, Inc. (PAYX) is confirmed to report earnings at approximately 8:30 AM ET on Wednesday, December 22, 2021. The consensus earnings estimate is $0.79 per share on revenue of $1.06 billion and the Earnings Whisper ® number is $0.83 per share. Investor sentiment going into the company's earnings release has 60% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 8.22% with revenue increasing by 7.76%. Short interest has increased by 0.2% since the company's last earnings release while the stock has drifted higher by 8.7% from its open following the earnings release to be 13.2% above its 200 day moving average of $109.45. Overall earnings estimates have been revised higher since the company's last earnings release. On Wednesday, December 1, 2021 there was some notable buying of 885 contracts of the $85.00 call expiring on Friday, January 21, 2022. Option traders are pricing in a 6.0% move on earnings and the stock has averaged a 3.4% move in recent quarters.

Blade Air Mobility, Inc. $8.56

Blade Air Mobility, Inc. (BLDE) is confirmed to report earnings at approximately 7:30 AM ET on Monday, December 20, 2021. The consensus estimate is for a loss of $0.14 per share on revenue of $13.50 million. Investor sentiment going into the company's earnings release has 45% expecting an earnings beat. The stock has drifted higher by 18.6% from its open following the earnings release. Option traders are pricing in a 32.4% move on earnings and the stock has averaged a 7.4% move in recent quarters.

Cintas Corporation $438.51

Cintas Corporation (CTAS) is confirmed to report earnings at approximately 8:30 AM ET on Wednesday, December 22, 2021. The consensus earnings estimate is $2.62 per share on revenue of $1.90 billion and the Earnings Whisper ® number is $2.78 per share. Investor sentiment going into the company's earnings release has 65% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 0.00% with revenue increasing by 8.14%. Short interest has decreased by 26.5% since the company's last earnings release while the stock has drifted higher by 11.5% from its open following the earnings release to be 14.2% above its 200 day moving average of $384.05. Overall earnings estimates have been revised higher since the company's last earnings release. Option traders are pricing in a 4.4% move on earnings and the stock has averaged a 2.1% move in recent quarters.

DISCUSS!

What are you all watching for in this upcoming trading week?

I hope you all have a wonderful weekend and a great holiday-shortened trading week ahead r/StockMarket. :)

")

")

- Part of the global Agenda")

")

![[link]](https://i.redd.it/3cryg1kikj681.jpg){kind=link}

![[link]](https://i.redd.it/aq2y3de1em681.jpg){kind=link}

![[link]](https://i.redd.it/q0vnjx4msc681.png){kind=link}

![[link]](https://i.redd.it/bbruefbv1b681.jpg){kind=link}

![[link]](https://i.redd.it/x7ieisg6ba681.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment