Financial Independence What’s the point of wealth? An excerpt from a book review in the news today. |

- What’s the point of wealth? An excerpt from a book review in the news today.

- Living within your means

- My path to FIRE....

- On not having fun, not making or losing friends, being a shut-in while pursuing FIRE.

- Stack Overflow annual survey Analysis: FI Perspective

- Teaching the next generation

- Intersection between FIRE/Lean-FIRE and Homesteading

- Daily FI discussion thread - April 12, 2019

- Keep normal IRA contributions (traditional or roth) and 401k rollovers in separate accounts!

- When did you achieve NW 0

- Weekly FI Frugal Friday thread - April 12, 2019

- Exercising Stock Options

- Learned FIRE after the fact

- Advice for FIREing in a HCOL City

- Financial independence and career change.

- Anyone Achieved FIRE in a Nonlinear Fashion?

- Megabackdoor vs Solo 401k

- One-time decisions with long term impacts

- Calculate FI with a lower paying/part time job

| What’s the point of wealth? An excerpt from a book review in the news today. Posted: 12 Apr 2019 09:44 AM PDT Early in my career I worked at an old fashioned savings and loan bank. We offered the best rates in town, and this attracted a certain kind of customer. One emblematic individual was Mr. Tonlin. He was meticulous in his management of his $4,000,000, which was divided among fifty or so accounts with different maturity dates. He would come in every week with his list on a clipboard held proudly to his chest and carefully make decisions about which ones to get, haggling with management for better rates. He carried the air of a business magnate from the Industrial Revolution. This was his pride and joy. Then, after years of this routine, his wife passed away. Mr. Tonlin came in the afternoon after the funeral—perhaps to get some grounding in his routines. He seemed like he had lost six inches of height. He came into the bank lobby expressionless, posture limp, disoriented. Various staff came up to him, expressing their condolences. He ambled to the counter holding his clipboard, which now seemed to be very heavy to him. We waited for him to say something as he looked at the list. Then quietly, looking down at his clipboard, his chin quivered and his eyes welled up, "I should have spent this money with her. What am I going to do with it?" It's been over a decade since this happened. I would bet that a week hasn't gone by that I haven't thought of that man and this single phrase. After telling my clients this story, I repeated the question to these trailer park millionaires, "What's the point?" I believe that those who have saved up deserve the reward of minimizing their fears about money while maximizing their energy for the real things of life. Ask yourself: what is the point? This is not a rhetorical question. If you and I optimize your financial life, leaving no stone unturned, what's the point? What would change? What should change? To me, the point is this: you should have the luxury of diverting your emotional energy away from worrying about money. Spend that same energy on more important things like family and friends, pursuing goals and experiences, enjoying life, or giving back to the world. The emotional cost of financial chaos is profoundly impoverishing. Bringing order to chaos will enable you to divert your energy to the things that enrich your life. Financial strength is not about having a lot of money. The ancient Romans had a saying, "Money is like seawater. The more you drink, the thirstier you become." As you grow in wealth, you must also grow in wisdom. Full post: https://coloradosun.com/2019/04/12/chad-gordon-wealth-by-virtue-excerpt/ [link] [comments] |

| Posted: 12 Apr 2019 08:19 AM PDT The last 2 months has been really eye opening on my path to FIRE. We lived in HCOL area for 8 yrs, managed to live in cheaper suburb (house was still $295/sq foot) and even bought a house in 2012 after the crash. We were on our way to FIRE in 5 yrs from now (42 for me and 41 for wife in 5 yrs) but couldn't take the rat race, sold house last yr and moved 4 hrs away. I worked in that smaller town since then and only last month accepted a job where I travel back to that same HCOL area twice monthly for a day of work. It has been eye opening! A few observations : -our quality of life is so much greater in our current smaller town despite making a lot less money and moving our FIRE plans back several yrs. - we spend more time with our kids and the family bond has improved. - The kids also have stronger relationships with their friends as they see their friends more often due to living closer and not having to worry about traffic (can walk or bike to friends homes even!) - we know and talk to all 80% of our current neighbors. - how unfriendly some bigger cities are, people look at each other less and don't always strike up conversations with strangers. - cell phones rule any public space - a lot of people appear to be making a lot of money but also appear to be spending a LOT more. This is not made to be a rant or generalization of the area. I loved the area while living there and still do. I just find it so interesting how my viewpoint on an area can change so much in such a short time. Also, I feel that I am looking into it as an outsider instead of being in the day to day grind. Just wanted to post as maybe a reminder that QOL if just as important while working towards a goal and not just focusing on the endpoint. I see a lot of posts about people who have nose to grindstone so much that they feel isolated. I see that in my old HCOL area. Hope someone finds something positive or helpful from this post. Happy Friday everyone! Edit : I can't comment on traffic as we both work in healthcare (physical and occupational therapy - rehabilitation, Wahoo!). My wife had 5 min drive to hospital and I had a 15 min bike commute to a clinic. This also makes work easier as therapy is needed everywhere and makes commuting your option. Edit #2 - we moved to a city of approx 125,000 people so not the sticks by any means. A college town! We have lot of arts, walk 2 blocks to coffee shops, independent movie theater, restaurants, etc. Bike 1.5 miles to downtown. The nightlife shits down much earlier than metropolitan area. QOL is very important to us and we have moved a lot over the yrs. U could say it took us 15 yrs to find what we wanted. I'm amazed at the number of responses here. Great to hear from everyone amd wish I would've posted something like this a few yrs ago [link] [comments] |

| Posted: 12 Apr 2019 09:44 AM PDT TLDR: hi. I'm new here. I've had a life and I'm sharing it with you because I'm bored today —— Relatively new to Reddit and have been stalking this sub for a few weeks. Thanks everyone for sharing your stories and a helping others with your comments. It's nice to find a corner of the Internet with like minded nice people. I feel odd sharing my experiences unsolicited. But it seems like people enjoy the conversation and hopefully someone will be able to cherrypick an idea or two out of here. Also, I'm a passenger on a cross country drive and I have time to kill. :) I'm a 43M married dual Income family w 2 kids living in a LCOL area. I could probably be FI now, but I like working and derive some part of my social life and self worth from work. Also the cost of 2 kids keeps our expenses high and our need for health insurance also incentivizes us to remain employed. To be fair to anyone reading this, I did get a good start off in life being an only child in an upper middle class family. I know for a fact that I got a better then average start in life, but I do believe that decisions made along the way contributed to where I am today.

Now that I'm here in life these are my struggles. At some point if you work hard and save a lot, you need to transition to the opposite. You need to back off work and enjoy (spend) that money. This has been hard. I could live to 100. I could be sick for 20 of those years. My rentals are a regular source of income, but they are always out there as a potential haunting expense. It's totally foreseeable that i could need to do a roof, a heater, evict a tenant that trashed the unit and have a basement sewage backup all in the same year (that was 2016). So I never really know if I can spend that money. My wife and I are occasionally on different pages. She works, enjoys her career and derives self worth from it. So I don't want her to quit. However, it's a normal job. Sick kid? She doesn't have the flexibility I have. And I'm super grateful I have it. But I feel very self conscious calling my business partner or an employee and canceling or rescheduling something they are counting on me for. It's kinda like "hey, I'm the dude who only works 25 hrs a week and yet I can't make this important meeting we've worked into 5 people's calendars weeks ago". (Warning: 1st world problem coming). I also struggle with raising kids. I read a great book "the opposite of spoiled" that made an interesting point. In some family's there is a natural balance in what the kids can and can't do. The family only has so much money and time. In other families, there are more financial and time resources. In such cases parents need to set limits. The problem is that those limits are arbitrary. My kid went to summer camp overnight for a week. He loved it. Next year he asked "can I go twice?" It's a win win. He loves it mom and dad get time solo with the other kid. Mom and dad love it. Other kid loves it. But, isn't sending the older kid to camp twice spoiling him? Many kids don't get to go to camp at all. Telling him once a summer is enough is probably what's right, but at its core it's arbitrary. Anyway. Some of this felt like I'm bragging. Hope it didn't come across that way. I've shared my story with others in person and some of them have picked up things and run. I think the core here is to live below your means (it's not possible for everyone so be fair to yourself), if your young try and share housing costs with others for as long as possible and bank the savings. And I think almost (almost) anyone at any age can get a second job. Thanks for reading. I still have several more hours in the car :) [link] [comments] |

| On not having fun, not making or losing friends, being a shut-in while pursuing FIRE. Posted: 11 Apr 2019 07:18 PM PDT There are many people here who describe losing friends, becoming shut-ins, and not having any fun as they work towards FIRE because everyone else just wants to go out to expensive dinners or clubs all the time. I find this pretty strange. Maybe I have just had quite different life experiences than others. Grew up lower-middle class. Paid for my own schooling. I've been 'living cheap' for years before finding out about FIRE. During this time I've had a few different living situations. Maybe we can have a discussion about how to find good people and situations. In school: I joined an engineering fraternity. Living in the frat house was not terribly expensive, and I was surrounded by people who were always messing around building electronics projects or lighting things on fire. It was great. Lots to do all the time, not necessary to spend tons of money. First place out of school: Shared an apartment with a bunch of people just out of school. Low standards, but we were all friendly and did stuff together. Second place: Cheap condo (Bought for $32,000, $0 down. Lol. Gotta love Rockford, IL). Made friends with some of the other condo residents, and people from work. Place was cheap because it was close to downtown and in a more dangerous neighborhood, but I never had any issues and I could go downtown to markets and the river bike path and whatnot. During this time I was being sent overseas for work all the time so I was having my fun traveling. Third place: Bought a house. Got a roommate - an engineer about my age from the place I worked. We ended up setting up a little maker lab in the basement. Our computers down there, a 3D printer, electronics kits. It was great! People came over and we did stuff together! Moved to Seattle: Holy shit what a cost of living adjustment. Rented a room in a house for a while to figure out how I would manage to live here. Eventually set up my current situation. I live on a small boat now in a trendy Seattle neighborhood, and have two shipping containers in an adjacent industrial yard. (Boat cost $4000, slip rental $430/mo, containers cost $2500 each, yard space rental $150/mo). In the yard, there are all sorts of weirdos with their own containers set up as shops and hangout spaces. Hippies, artists, craftsmen, drunks. There is a working art foundry, wood shops, a glass studio, and a communal compound made of stacked shipping containers where we have shows and parties. For me, these were the kind of people I've been waiting to find. Always interesting, super community minded, friendly. Between the marina and the yard, we have cookouts together all the time. Some people bring meat, some bring veggies, some bring alcohol. Its good cheap fun! When we do go to a restaurant, we eat 'family style' at places that aren't family style. We'll buy two appetizers and two dinners for six people and share around. I dunno man, we're shameless I guess. Maybe other people would cringe at this, but whatever. We go to the same places often and know the servers and they like us. How did I get into this? I just decided "I want to live on a boat. What do I need to do to make this happen?" That led to me visiting different marinas, meeting people, finding out about Seattle industrial yard culture (lol), buying a boat, getting to know the marina manager well, getting liveaboard permission from the marina, getting space in the yard, buying a container, etc. What I would say to take from my experience so far is that there are so many different types of people out there who do not want to spend money at the bars, and you have to look for them. In my opinion, by chasing interests and OFFERING TO HELP. Seattle examples: I could have started with an area maker lab, then found Equinox Studios in Georgetown, talked to people there, helped someone out with art/industrial projects and shows like Dead Baby and Georgetown Art Attack/Equinox Open House.. Or starting with Fremont Arts Council and volunteering on a Solstice parade float, then getting involved with Moisture Festival, then making an exhibit for Science Night at Hale's.. Or volunteering at the Center for Wooden Boats, getting to know the full time volunteers, getting to know the volunteers on the other historic boats, hanging out with them watching the sunset over Lake Union from the deck of a 130 year old tugboat. I do all this stuff. None of this costs real money! When I was hanging out with the boat volunteers (who ranged in age from 20's-50's in case you are curious), we walked to a grocery store, bought some cheap food and alcohol, and made dinner together on the boat! That was our night out and it was plenty more fun than a loud expensive bar. I'm not a 'cool' guy or an awesome artist or anything. I (very) often feel that I'm not interesting enough to be part of the groups that I'm a part of. But I show up and contribute and am positive. And I have tons of cheap fun! Is this helpful? [link] [comments] |

| Stack Overflow annual survey Analysis: FI Perspective Posted: 12 Apr 2019 07:04 AM PDT Stack Overflow just posted its yearly survey results. For those of you who push development so much, I think it's a worthwhile read: My key takeaways as it pertains to this sub:

My conclusions: Software development is a great career that many of us take part in one way or another. However, many of the above statistics back my feeling about pushing development as a job onto people in this sub (huge confirmation bias warning). My biggest takeaways are that the people who are geared for the job are already in it. The statistics back that "just learn to code" doesn't succeed often, and the older you are it's even more unlikely. In addition, y'all need to stop pushing the "6 figures out of college being common" myth. These are the median salaries across all of the roles in the survey. The US market is clearly higher paid than the rest, but even so, the median is just barely above 6 figures, without taking experience into account. The vast majority of respondents have been professional developers for more than 5 years (only 13.4% of devs have less than 5 years of professional experience). "But what about FAANG, those guys make bank!?" The median tenure at Amazon in the tech world is 1 year. Their RSU vesting schedule is 5%, 5%, 15%, 40%. That means most of these workers will see only 5% of their RSUs, which is where a large amount of the compensation numbers you see comes from. Google has a median tenure of 1.1 years. Apple is the best among them, at 2 years! I love my job, and it has set me up for a great start to FI. I teach JS/HTML in my free time because I think it's a great hobby, plus I can maybe persuade some younger people to get into the job and find their passion there. However, this sub has pushed coding as the best way to make it without regard to the individual's passions or abilities. I also feel that there is a lot of misinformation about the career prospects for a non-formal approach to development. There will always be outliers that will prove it is possible to do so, but the statistics seem to back my vantage point that it's not as easy as people make it sound. I truly believe the key to success in tech is passion and motivation for technology. Updates after initial comments:

Sources 2019 Stack overflow survey - https://insights.stackoverflow.com/survey/2019 Tech worker tenure - https://www.forbes.com/sites/forbesbusinessdevelopmentcouncil/2018/06/29/the-real-problem-with-tech-professionals-high-turnover/#f7c6f8242014 Admitted flaws in my logic

[link] [comments] |

| Posted: 12 Apr 2019 10:26 AM PDT Having some great discussions in our family about FIREing the next generation (at least FI). What're your stories? My 9yo started her first job recently. While we do not pay for family chores that are part of the day-to-day for the household, we do have some nearby property that needs mowed and generally is "extra". A few weeks ago she started mowing that lot and we made a deal where I would pay her if she agreed to a commitment to save it for retirement. Her first day, the neighbor adjacent joked "Hey, when are you gonna come mow mine?". This week, she knocked on their door and got a gig mowing for him. Somebody else just posted to a community chat that she was new to the neighborhood and wondered if any kids around here were doing low-cost lawn mowing, and my daughter's ears perked up. She has a business meeting for it after school today. This has led to age-appropriate discussions about compound interest, retirement, and using Excel (she's doing a lot at school in Word and PowerPoint so this is a natural extension. How excited she was to learn there was a program on her computer that would do her math for her!) I showed her that she could be a millionaire if she made the Roth Max in contributions every year from now till 18 by ~44, and that if she did nothing between now and 18, she couldn't catch up to ~10 years of saving now and never again contributing after 18. We track all of her business income for tax reporting and I've shown her a simple formula to separate out e.g. gifts as they're not eligible for her Roth IRA. We're using Fidelity and I was just thinking we'd land her funds in VTI when she got her balance high enough but today I found FZROX. I can't wait for her to get home from school today so that I can tell her she can start owning a little piece of Apple and Warren Buffett's company by end-of-market on Monday and can actually buy securities $10 at a time instead of waiting to accrue $150 for VTI and then pay $5.95 for transactions. My wife told her she was proud of her hard work and commitment even though lawn mowing is tough and it's hot work that's not always her idea of a fun Saturday. My wife lamented that HER dad had never told her about saving for retirement, and my daughter replied "Hey, dad? Are there any things you're not telling ME?" We'll have to save the discussions about FIREcalc and MonteCarlo simulation for a bit, but I'm hopeful she'll be FIRE well before I will, age-wise. [link] [comments] |

| Intersection between FIRE/Lean-FIRE and Homesteading Posted: 12 Apr 2019 07:44 AM PDT For the most part people seem to take "Financial Independence" to mean "be a multi-millionaire in my 30's" which is not practical for the vast majority of people even in the wealthy West. This is a dream of becoming "independent" by having lots of money to buy the necessities of life from other people. I don't see too many people dreaming of living on a small farmstead and becoming independent by being more self reliant. Admittedly it is not a glamorous life, but via my wife's family I know a woman in Eastern Europe in her 90's that has been financially independent practically her entire life. At one time she and her husband were dairy farmers but he passed away 20+ years ago and since she has lived on her 40 hectares of land as a small farmsteader. She chops wood right in her kitchen to heat her home with a wood burning stove in the winter. She keeps chickens and a goat and has many cats and several dogs. Seemingly the physical labor necessary to maintain this farmstead lifestyle is partly to thank for her longevity. I don't think she ever worked a day in her life outside of her family farm. Is that not true independence? She receives a small pension from the government and gets some E.U. money for various things she does or does not do with her farm. What do you all think about this form of financial independence via self reliance? Or do I misunderstand what FIRE stands for? [link] [comments] |

| Daily FI discussion thread - April 12, 2019 Posted: 12 Apr 2019 01:08 AM PDT Please use this thread to have discussions which you don't feel warrant a new post to the sub. While the Rules for posting questions on the basics of personal finance/investing topics are relaxed a little bit here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Have a look at the FAQ for this subreddit before posting to see if your question is frequently asked. Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] |

| Keep normal IRA contributions (traditional or roth) and 401k rollovers in separate accounts! Posted: 12 Apr 2019 08:20 AM PDT Just thought I'd post this, as a couple of posters asked why this should be done. (Sources included at the bottom) Both 401ks and IRAs offer substantial protection during bankruptcy proceedings, but 401ks offer substantially more protection, and those protections apply to funds rolled over into IRAs as well. Ideally this would never be an issue. We as a subreddit are better about saving and investing than most people. We probably aren't going to have as many bankruptcies as the general public. But sometimes life throws giant curveballs at you, and if shit hits the fan it's better to be protected as much as possible. IRAs protect ~$1.4 million in assets, per person, not per account. Someone with $1 million in a Traditional IRA and $1 million in a Roth IRA, funded entirely from normal IRA contributions, could lose ~$600,000 from those accounts if they declared bankruptcy. Also, while you might intend to retire with a partner and say $1.5 million total in your IRAs, ideally that money grows even while you're retired, so it could cross the protection limit in the future. 401ks do not have a limited amount of protection though. If you have $10 million in a 401(k) and declare bankruptcy, you will get to keep all of that $10 million. The same protection applies to 401k funds rolled over into IRAs. If you rollover $4 million from a 401(k) into a Roth IRA, that $4 million (and the gains from it) would be completely protected. They would still be protected even if you rolled them into a Roth IRA that you have made Roth IRA contributions to, or that you have funded with Traditional IRA rollovers. However...in accounts with mixed funds, the court must determine what percent of the account is attributable to the 401k funds and what percent is attributable to normal IRA contributions. Ideally, the numbers end up being what they would have been had you kept the funds in separate accounts to begin with. However, courts are slow, and it takes time for them to do anything. Time is money. Much easier and cheaper to just keep the funds separate from the beginning! Again, only really an issue if you end up having to declare bankruptcy, but we don't know what the future holds, so why not give ourselves as much protection as possible? Edit: On mobile so I don't have my bookmarks, but here are some sources. A little out of date in how much IRAs protect but: Retirementwatch As much as I hate LegalZoom this also appears accurate, second source: Legalzoom Source 3: Random financial advising group

That's actually news to me. I'm not an ERISA attorney but I'll look into that this weekend. [link] [comments] |

| Posted: 12 Apr 2019 04:28 PM PDT Looking at my financials, and before a 401 I forgot about, I'm teetering on a net worth of 0, so I was just wondering how old you were when you achieved the same. [link] [comments] |

| Weekly FI Frugal Friday thread - April 12, 2019 Posted: 12 Apr 2019 01:08 AM PDT Please use this thread to discuss how amazingly cheap you are. How do you keep your costs low? How do become frugal without taking it to the extremes of frupidity? What costs have you realized could be cut from your life without pain? Use this weekly post to discuss Frugality in general. While the Rules for posting questions on the basics of personal finance/investing topics are more relaxed here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] |

| Posted: 12 Apr 2019 02:10 PM PDT Was wondering if any of you have experience with exercising stock options. Notably, did you exercise and wait a year to get long term capital gains? Did you borrow the money to exercise? For those of you with a large initial exercise cost, where did you find the money to purchase them? [link] [comments] |

| Posted: 12 Apr 2019 03:39 PM PDT So I am going to be 34 this year. From about the time I started working I have been saving and investing in my 401k. I got about 100K in my 401K and 110,000 USD saved. I decided to buy a house now so I put 20% down. Reading more about FIRE is making me think I made a mistake... I bought in a city so I know I will get my money back and then some, or at least there's a reduced chance I will lose money after x years. I'll have about 40K left. I am thinking I will continue to do 15% on my 401k, but will start investing my extra cash into Vanguard because I don't want to wait until I'm in my 60's to retire... did I screw myself over? I've always had a feeling the market is gonna crash but it never really did... and I've waited too long. If I would have stepped in 1, 2, 3, or 4 years ago I would have been ahead... sigh.... [link] [comments] |

| Advice for FIREing in a HCOL City Posted: 12 Apr 2019 11:43 AM PDT I (21F) just got offered my first job out of college and will be moving from a LCOL Midwest city to Seattle following my graduation. I have wanted to live in the Pacific Northwest for a while and definitely would not trade this opportunity for the world. However, I am concerned about what my spending rate will look like in a city like Seattle. I want to enjoy it and plan on going to the parks in and surrounding the city pretty frequently as my main form of entertainment. As far as housing goes, I really do want to live in the city for the first couple of years and am comfortable with paying 1,200 a month if it means I am close enough to walk or bike to work and can avoid transportation costs/headaches. My first year salary is close to 70k after bonuses are paid and when my husband finds a job there I'm expecting we should be able to have a gross income of about 105k. I already created a rough budget in excel of what I expect all of our costs to be around and even budgeted in the costs for fun activities for us like trying new restaurants a few times a month or traveling expenses to go to nearby national parks. All things accounted for, our estimated savings rate is 60% with monthly expenses of around $2,750. I have no idea if this is a good savings rate (or maybe it is unrealistic for Seattle?). If you live in a HCOL city please add in any tips you have for avoiding high expenses and also maybe some fun things to do for free. Also please make me aware of any expenses I may be missing as I've never lived in a big city before and am basically starting "real life" for the first time. By the time my husband and I move we will have paid off all our debts and have about $5,000 in savings after moving expenses and first months rent + deposit is paid so we won't have to worry about student loan repayments as a part of our budget either. I'm excited to get started on my FIRE journey and appreciate any feedback you have to offer! [link] [comments] |

| Financial independence and career change. Posted: 12 Apr 2019 12:30 PM PDT Also posted on r/careerguidance but figured many of the people that have similar careers visit this subreddit and might be of help. Please let me know if I should remove it. At 27 I've decided to go back to school to pursue a bachelor in Accounting. To give some background, I moved to this awesome country right after turning 21 and I come from a third world country. I was lucky enough to get a very good starting job (around 40k year) but not knowing anything about how being a grown up worked I put myself in some debt and didn't make many conscious financial choices. Tried college for Business Admin. but found it to be a total bore so ended up dropping out after first semester (all the wrong reasons, I was lazy and made a dumb choice) but I spoke to them recently and they said I can pick up where I left, "just come in and re-apply". I currently have a pretty good job (low 100's) that will allow me to support myself and pay my full ride through school. (Associate would be around 3k per semester with a pathway into an accredited university and finish my bachelor for around 9k per semester). Problem with my current job is that it has an expiration date (won't be able to do it after a certain age) and it comes with some serious burnout. I'm hoping my 30th birthday will be the last I celebrate there. My goal is to: maybe become a CPA upon graduating and/or if my brain is not failing me and I discover I can take it I might look into becoming a tax attorney. I'm also open to explore similar career options like wealth management and financial advisor. My fears? I'm 27! I'm scared it might be too late for me to have such an ambitious dream. They say you can do whatever you set your mind to but realistically age can play a big role in career making or breaking. Also salaries in this industry vary greatly so I always wondered what would be the best call for someone starting late in life who can't really afford much time to "figure things out", not looking for a shortcut but would like to make smart choices with the time I have. As someone in search of FI no RE potential earnings are very important along the lines of doing something fulfilling. Anyone been in my position and succeeded? What advice do you have for me? Should I go for something less complicated and if so what? What has been your experience with going back to college later than usual? Anything would be appreciated. Worth mentioning I'm also single with no dependents. All the responsibility falls on me and no partner or parents (or family in the US) for support if things get tough. Not saying it's an obstacle but it does make things a bit scarier. TL;DR Want to start career in accounting but scared because I'm 27 and not sure if it is the smartest financial idea or if a good idea at all. [link] [comments] |

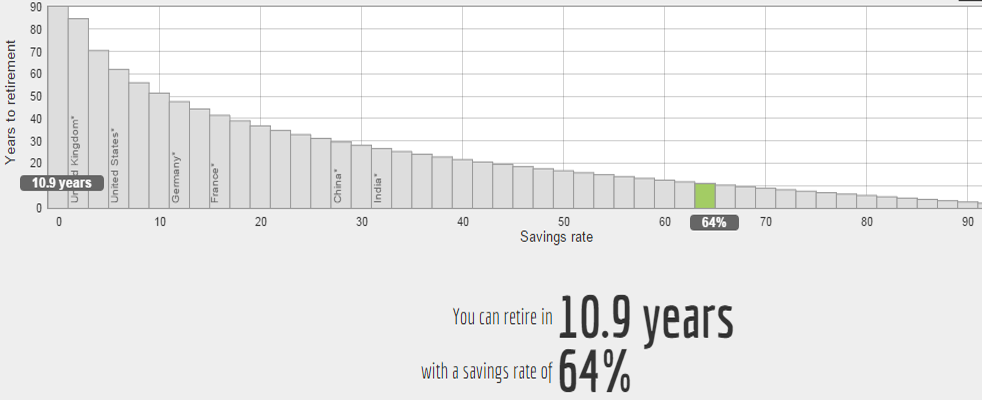

| Anyone Achieved FIRE in a Nonlinear Fashion? Posted: 12 Apr 2019 10:53 AM PDT Hi all, For those that have achieved FIRE in a nonlinear fashion or have taken interesting detours and are still trying to achieve FIRE - what has your journey looked like? How have you been able to recover from a momentum loss from an extended break? --------------------------------------------------------------------------------------------------------------------------- The average mantra of "work until 65 then retire" seems rather linear. So does the "grind and save 64% of your take home pay until 30 like Mr. Money Mustache's graph, invest, then retire, decompress, take your first vacation, then find more fulfilling work on your terms" mantra of the FIRE community. There is another nuance in the FIRE community: not everyone can be $100k a year software developers like Mr. and Mrs. Money Mustache. It'll take longer with jobs that pay less. Along with changing local real estate economies that can make a home buy a nightmare if the area tanks. ------------------------------------------------------------------------------------------------------------------------- In my experience, life isn't linear. You lose a job, get a new one, get burnt out, make a bad investment decision, etc. Willingly (or unwillingly via job loss) taking an extended break (6-12 months) seems to be out of the question in the FIRE community (from what I've seen). The break could be to think harder about your purpose, recover from burnout, or you lost your job and are forced to break. -------------------------------------------------------------------------------------------------------------------------- Here's my story: My father was a painter (spring/summer/some fall) and built/rented/renovated homes. He and my mother have their MBA's, but have never worked for someone else. My dad graduated university and barely bought his first home for $12k, renovated it and sold it for $36k. At the time he figured, why the heck would I want to work some corporate job for someone else? He didn't know (at the time) that he got lucky with the economy picking up. Fast forward - as a kid I've always worked with my father painting, digging ditches, renovating homes, etc. My working hours with him extended at 10 years old onwards. I remember all his tenants would leave the house a mess. My dad was too generous. He has only been to small claims course twice in his 30+ year landlording career. Turning over the homes was always a pain because of his kind heart. Cutting out carpet with a box knife b/c the tenants let their cats piss all over the floor. Garbage all over the front/back yards to pick up. Digging ditches in the rain for the plumber to lay his pipe, sweeping floors, making dump runs, etc. I didn't have a job in high school, but instead always had one with my dad. I did pretty well in high school - martial arts freshman to junior year, swimming and crew junior to senior year and ASB president for my entire school senior year. 3.44 GPA. My mother never came to any of my sporting events. My father never provided me guidance, but came to the martial arts events. It seemed my college was already chosen for me. My father, grandfather and many family members went to this private university. What is sad is that if my dad supported me I could've been a rower at an elite rower at this prestigious university. I still kick myself when the coach could've gotten me in for rowing. But...I didn't take it. I didn't know how to think for myself. I was always "guided" by my mother and avoided by my father. No one in my family even cared to ask about how my regattas went. It was always about them. College hits - I start window cleaning for College Pro for a few months in the late Spring of my freshman year (3 months). First time working for someone other than my dad.

As college concludes:

Unemployed for the first time ever (when I started working I stopped helping my dad - he understood) I had no clue what to do or what I wanted to do. It was jarring. I didn't even think to travel because I was so into the mindset that I had to achieve. I later learned that was because I always wanted to earn the love of my parents. I later learned they were narcissists. They had a limited capacity for empathy and love. The most sobering realization of 2018. My mother kept pushing me to get a college job. I graduated a quarter early and walked in the June. I thought I could rest, but she kept pushing and pushing. It was as if she didn't want me to travel Asia for (6) months by myself like my sister did (2 years younger than me, same university). I later learned she didn't want me to have independence. She wanted me under her thumb. Long story. Corporate Career:

Life After Corporate America This all took place within (3) years. And I have to say I was miserable every second of it. I put on so many masks to fool myself into liking what I did. I adapted to so many different corporate cultures I was exhausted. When the mirror broke I was devastated. In the context of my whole life, I am a duty bound and ambitious man. For example, the main Fortune 500 company decided to poach me two months into my last corporate job. I was so grateful of being hired out of a bad last job to a chill manager that my loyalty did not match reality. I declined and told my boss that I did. Looking back - I probably should've taken it. But then again I took an Adrenal Test and was burnt out. I wouldn't have last in even more demanding company that I was fired from initially in Job 1 given my energy levels. Choosing to leave was like committing mental harakiri. I took such a hard emotion and psychological blow. The grief was almost unbearable and I had no one to help me through it. But there was no shortage of people that wanted to kick me while I was down. THIS TIME I did tell my parents the truth before I quit. This time I did tell them that in two months after quitting I was going to see all (50) states by myself (I've already been to Alaska/Hawaii). And holy shit did they use every single person I ever met in my life to try to get me from going on this trip. No love. Absolutely getting ignored. The dog doesn't get any treats when he doesn't do what the master wants. I cannot tell you how I was attacked on so many angles by so many people in my life. I chose the USA because I felt it was wise. I went through all this trauma that the extra stressor of having to learn another language/system would push me overboard. I also wanted to learn more about my country of birth especially under this polarizing presidency. I've also realized I've been everywhere else except my own country. Time to pay homage. And lastly, I realized if I was to make any serious money (I am a realist as well as someone seeking fulfillment) the best system to do it is the USA. I went against the American ideals embedded in my family - business is a virtue, if you're not working you are worthless, internal achievement pales in comparison to external achievement, travelling your own country instead of another country is uncultured and intellectually lazy, etc. Cousins and friends alike laughed at my decision. And my God did I feel the heat. But I announced a date in advance. I could've left in the middle night like a coward when my parents were aboard. However, I stood my ground and left with dignity. My mother hated it. We are no longer in the third world country she grew up in. She chose America and got her citizenship the hard way (not through marriage). She also chose American defiance, ingenuity, freedom, and the right to pursue anything within the law. Little did she know that that system allowed her son to live a life absolutely free from her control. The system of the old world would have allowed her to have such a tight grip on me. And here I am. Living in the first real major choice of my life. Unlike my corporate career, I wasn't pushed and manipulated into it by my mother. The massive resistance from every single person in my life tells me it was all against their interests especially my mother. And that makes me feel like this choice is truly original - uninfluenced by anyone. Call it selfish. Call it self compassionate. It depends on your perception. To summarize, before I left:

It's been (8) months of travel across (23) states by car. It's been a true journey. My dual goals are to seek purpose and a new place to live. I have a list now. It's just time to seek more clarity to make a real choice. It's been eye opening to say the least. Solo travel is different when: A. You are under massive trauma from job loss, family emotional abuse, a hostile work environment, adrenal fatigue/stage 4 burnout, a few betrayals from friends before departure. B. You are not with a tour group or family to filter how others treat you. Despite having traveled all over the world, it is like I am seeing the world for the first time. And boy is it stressful. I do have fun, but again I have been focusing more on exploring myself, the USA and healing. C. You are looking for an entirely new place to live. D. You are looking for an entirely new line of work. E. You have absolutely no approval from anyone in your life and all the resistance in the world. F. You are absolutely alone on your journey. Not exactly relaxing. I did have some resources others didn't: A. A house that generates $31k gross income a year w/ no mortgage. (Although unlike the car the title is not in my name. My parents wouldn't do that because if they pull my inheritance it would give me full reason to make a completely clean cut. Also, it would invalidate all the legal battles they fought from those trying to sue them for their wealth in order to control them and their decisions). B. Saved $70k since I mainly lived with my parents, don't drink alcohol, don't drink coffee, and don't do any drugs. C. Have a credit score of 823 out of 850. D. Had COBRA from quitting work for health insurance. E. Had a Health Savings Account (HSA) that I saved $6k+ in for acupuncture (surprisingly an eligible expense) or other health problems. F. A car fully paid off that I've had for a decade (family gift at 16 if you want to count that privilege against me for any reason). But privileges aside, you can see I work like a dog and have certainly been treated like one. I can live off this income indefinitely. I know how to cook. I am excellent with a lot of FIRE principles. Reducing expenses is easy for me. I slept on the floor for (3) years from Junior year in college into my corporate career. I have been practicing 1-7 days of fasting (mainly intermittent fasting) since Sophomore year in college. But simply having FIRE is obviously not fulfilling. I am grateful I have achieved it. However, I want to achieve more. My next step will be to get back into the game somehow and in a more fulfilling line of work. I will have the power of FIRE and the newfound business ability to walk away from any negotiation/situation (I walked away from everything I knew and love. I managed to survive the grief - what not could I walk away from now?). And maybe in another three years (if I don't choose correctly or disaster occurs) I take another (8) month travel break. I wouldn't want to. I would love to just find my purpose and not worry about it. But life isn't linear. It is pretty non-linear. What's your story? [link] [comments] |

| Posted: 12 Apr 2019 07:17 AM PDT Hi all, My wife and I are in our late 20s and currently max all tax advantaged accounts available to us. This includes: 2x backdoor Roth IRA, 401k w/ 50% match, Megabackdoor 401k, and HSA (includes 2k employer contribution). This puts our retirement savings contributions at about 70k per year. We currently have about 240k put away for retirement and is roughly roughly 50/50 in terms of being pre and post tax. All of these accounts are through my employer, and my wife is a 1099 contractor with 0 benefits. We have been toying with the idea of her opening a solo 401k, however we don't think we can max both the megabackdoor and the solo 401k at the same time. If we were to choose, which one should we prioritize in maxing? Are there reasons for maxing one over the other aside from being taxed now vs later? One thing to note is that my megabackdoor is currently invested in my employers 401k that offers funds that have an even lower expense ratio than public funds such as VTSAX. I believe the one I have is around 0.02% Our Target retirement date is around 15 years from now if that matters! Thanks all! Edit: My employer matches 50% of contributions, not 50% of income. [link] [comments] |

| One-time decisions with long term impacts Posted: 11 Apr 2019 06:31 PM PDT 25M, single, living in HCOL area and just passed $100k net worth!! In the middle of deliberating between a few future living options for the next year:

I just made the decision to go with option 3. It feels great to know I'll be saving between $500 and $1000 a month for the next year adding up to $6000 to $12000 in the next year based on one decision alone. That money, when saved, then invested and compounded over the years, will have a huge impact on my FIRE plans. Just thought I'd pass this along to remind us that decisions we make now can have lasting implications (hopefully positive ones) down the road. [link] [comments] |

| Calculate FI with a lower paying/part time job Posted: 11 Apr 2019 05:25 PM PDT I have searched, but not had any luck finding a calculator that allows you to see your target # if you have other income like rental property, or a part time job. How should I adjust my calculations based off 4% withdrawal and eventually fully retiring? [link] [comments] |

{kind=link}

{kind=link}

| You are subscribed to email updates from financial independence / early retirement. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment