Financial Independence Daily FI discussion thread - Sunday, May 09, 2021 |

- Daily FI discussion thread - Sunday, May 09, 2021

- Blue Collar & Working on FI

- How I tried to time the market in 2020 and I failed miserably. Hard reality check

- Do you know any secret multi millionaires?

- If you were <5 years from planned retirement, what would you be investing in today?

| Daily FI discussion thread - Sunday, May 09, 2021 Posted: 09 May 2021 02:00 AM PDT Please use this thread to have discussions which you don't feel warrant a new post to the sub. While the Rules for posting questions on the basics of personal finance/investing topics are relaxed a little bit here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Have a look at the FAQ for this subreddit before posting to see if your question is frequently asked. Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] |

| Posted: 09 May 2021 10:02 AM PDT I've been thinking about posting this for a while, but haven't really had the courage to do so. There's been many posts throughout the years wondering where all the posts from normal people and/or blue collars are. Well - here is one. (I don't write particularly well, I'm just very matter-of-fact). I went to a vocational high school and enrolled in Plumbing / Pipefitting. I graduated in 2007 in a dead economy. I was unable to find work as an apprentice, but eventually found work at a local plastics manufacturing company in the tool & die shop. I was paid $11/hr as an apprentice to mold makers and to do facility maintenance work for the shop. I worked 10 hours Monday - Friday, and a half day Saturday. I was entitled to 401K and tutition reimbursement (with no payback requirement or term of service). Matching contributions were frozen until the economy started to pick up, but I contributed as much as I could. ESOP company, so I got profit sharing (based on my salary) every quarter, which I never spent and put into a separate account. These amounted to 4 additional paychecks every year (if we did well). I enrolled in a community college which had an Engineering transfer program. I had to take a lot of remedial math courses to get up to speed because of my High School program. I took advantage of tuition reimbursement, and then took the reimbursements and put them into a Roth or Brokerage at the end of each semester. I remained at home and paid my mother $300/mo for my room. I drove a car I bought for $4000. I'll get blasted for living at home, I'm sure, but it was mutually beneficial. I was raised by a single mother who worked 60 hour weeks to keep a roof over our heads (I have a brother). There was no inconvenience. Working the hours I was working and going to school part time meant I basically needed a bed. If I wasn't at work, I was in the library, in class or sleeping. I did take a couple vacations/trips during this time during school breaks, but they were not extravagant. I learned to be very efficient with my time. I left this job in 2012 making $13.25. I joined a field service company maintaining specialized industrial equipment as a greenhorn for $17/hr (I was 23). This came with a company vehicle. I traveled all over New England and am based from my home address. The majority of our work is in greater Boston, which meant I was home everyday. I finished my Associates Degree program in engineering in 2014, and was given a pay raise to $25.00. At this time, I moved out (25). I lived with a girlfriend for a while (split costs), with a friend for a bit, and then eventually got my own apartment. My Community College had transfer agreements with some private colleges and the state university system. I was accepted into a few for Mechanical Engineering, but it didn't really seem to justify leaving my job over. I enrolled in a night program for Engineering Technology at the state university. 401K (6% matching), and tuition reimbursement strategy remained the same. I completed my Bachelor's in 2019, and was bumped to $34/hr. I currently remain with this company and was recently given a raise to $43/hr and primarily work on projects and technician development. I remain in the field and get my hands dirty on a regular basis, and no, my body isn't beat. I work anywhere from 28-60 hours a week depending on the season, but am guaranteed 40 hours of pay per week. I wish I kept more data, but the strategy that worked the most for me was just saving whatever extra money I got and then putting whatever raise I got straight into my 401k. If I didn't have it, I didn't miss it. At the end of every month I took whatever was left in my checking account and transferred it into my brokerage account. I'm still living on around $35-40K a year, but I'll treat myself - I just don't require much. I'm super minimalistic, but a couple of years ago I bought a personal vehicle, not important but it's a totally unnecessary expense. Currently single and 32 years old. Balances: 401k - $238k (target date funds) Roth - $77K Brokerage - $92K Plain old cash - $25K Total: $432K This past year my mother passed away, so I just recently moved back into her condo which was about 2/3 paid off (approx 180k, which I'd be entitled to half, but for now my brother and I are going to keep it). She left no debt. So now I guess I'm over $500k, but I'm not really counting the condo as of yet. Feeling pretty good heading into the future. Thanks for coming to my Ted Talk, you can do it too. [link] [comments] |

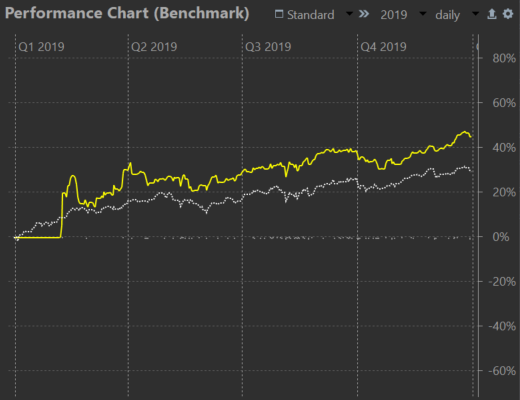

| How I tried to time the market in 2020 and I failed miserably. Hard reality check Posted: 09 May 2021 12:21 PM PDT I know that I'm preaching to the choir but don't make my mistake - this is a throwaway account to show you that timing the market will fuck you over. It is also a post to keep me in check for my future self. I can't believe I was so so dumb and I'm ashamed of my trades every. single. day. A bit of background about myself, I'm a 31 years old guy working in finance with a complicated past. My parents were not the best parents in the world, they had a drinking problem, I got my fair share of ass-whooping, and my self-esteem was always very low. Now take this extreme anxiety with a very doomer vision of the world and you got a recipe for a disaster. Fast forward a couple of years of blood, tears, and sweat and I landed a good job in an investment bank. I'm not a trader nor a PM but I do some middle office stuff for a couple of years now. I know how to read 10-k, financial statements, I do listen to earning calls and I know my fundamentals. I was always afraid to invest in the stock market having flashbacks to 2007 but I knew it was the only way to make money and I needed to do it before the world goes to shit. I knew I had to strike gold to become rich because with my salary I would never be able to prepare for the incoming floods, droughts, migrants problems, brewing civil war, peak oil and peak copper. I wanted to make money like those guys in WSB, like the btc miners and the RE moguls from 2013+. I wanted to reach FIRE as soon as possible not in 10-15 or 20 years In 2018, after 4 years of job-hopping and pinching every penny, I was finally financially stable to allow myself to invest and trade. My strategy was to select a couple of stocks to hold and a couple to trade. I told myself there's no better time to invest and I started investing in 2019 just after the 2018 dip in a diversified portfolio of growth and blue chip stocks with a 10 years horizon. It took me dozens of hours of research to select the stocks, reading reports and checking historical data. In 2019 I finished the year with a nice 15% pp above sp500 and I was really happy and flabbergasted by my ability to pick stocks. In hindsight, I was dumb and I followed to the T the Dunning Kruger path. 2019 was a bull market and it didn't occur to me I could just pick any stock and make money. picture Then 2020 rolls around and I started selling my portfolio. I knew about covid around dec. 2019 and I was thinking I can time the market. I thought it is my golden opportunity to strike gold. Just before Powell announced QE I decided to jump all in with a 2x inversed sp500 ETF AND VIX etf. It was my biggest failure... I stuck with those for a couple of months thinking that the market will eventually crash. How long the US can keep up with a 25% unemployment and one 1200$ check? Then I started doubting my strategy and luckily I started buying back my picks while selling the inverse and vix. And this is how I finished 2020 with -7% returns compared to 15% of sp500. 2020 performance chart YTD 2021. What can I say, my blue chips are crashing hard. Sp500 is at +15% YTS while my portfolio is -16%. 2021 YTD Overall, since 2019 I'm still +15% but it is nothing compared to sp500 I hate myself, I hate my life and I don't know what to do. I keep reading about people without zero financial knowledge getting +200% or 1400% returns after investing in April 2020 and here I am weeping and trying to understand my mistakes. When I look at my portfolio where I tried to time the market I just can't believe how dumb I was. I now have like "PTSD" symptoms and I will not invest any more money into the stock market. Inflation is eating away my money and I need to make peace with the fact that I'm dumb. Since 2020, fundamentals jumped out of the window, every person is investing and nothing makes sense. If I see another comment "It iS prIcEd IN" or how someone yolo'd everything into Tesla I will strip naked and run a marathon on the highway. I just can't bear with the fact that I have a master's in finance and I failed miserably compared to some teenagers that know nothing about EBITDA or FCF. My failures:

As I said, don't time the market, invest your money in VTSAX. [link] [comments] |

| Do you know any secret multi millionaires? Posted: 08 May 2021 07:16 PM PDT I was wondering if any of you guys know of people who live in humble living situations such as a condo and drive a $20K car but maybe are worth somewhere in the $8-$10 million range? I am sure there are people like that but I personally don't know of any. I would to hear stories if you are someone like that or if maybe you know of people like this. [link] [comments] |

| If you were <5 years from planned retirement, what would you be investing in today? Posted: 09 May 2021 02:56 PM PDT If you were less than 5 years from your expected RE date today, what would you be investing in? This is my situation, and these are my thoughts:

With all that said, what would be a good way to continue investing today if one was targeting retiring within 5 years? How would you hedge in order to avoid a disaster like retiring into a 50% drop? Apologies for any English mistakes. [link] [comments] |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| You are subscribed to email updates from Financial Independence / Retire Early. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment