Stock Market - Stock Market Meme |

- Stock Market Meme

- Many value stocks are up, while ORCL shoots up due to earnings

- $100,000 raised so far! Activision Blizzard workers announce open-ended strike and union drive

- PYPL - Why is PayPal staying down?

- Here is a Market Recap for today Friday, December 10, 2021. Please enjoy!

- Wall Street Week Ahead for the trading week beginning December 13th, 2021

- Most Anticipated Earnings Releases for the trading week beginning December 13th, 2021

- The Snowball. Before this book was written, Warren Buffett rejected numerous approaches by biographers, journalists, and publishers to cooperate on an account of his life. Here's a few lessons pulled from Alice Schroeder's work.

- FRIDAY RUNDOWN: AMC, GME, ISIG, PPSI, CEI, VSTA

- Last 24 hours based on mentions in reddit.

- Internet Psychology 101

- (12/10) Friday's Pre-Market Stock Movers & News

- Morning Update for Friday, 12/10/21

- The time to grab some GRAB is now

- The US government is asking Tesla why it lets people play video games while driving

- Tesla Under Fire For Allowing Drivers To Play Games While Driving

| Posted: 10 Dec 2021 02:35 AM PST

| ||

| Many value stocks are up, while ORCL shoots up due to earnings Posted: 10 Dec 2021 01:36 PM PST

| ||

| $100,000 raised so far! Activision Blizzard workers announce open-ended strike and union drive Posted: 10 Dec 2021 11:40 PM PST

| ||

| PYPL - Why is PayPal staying down? Posted: 10 Dec 2021 04:57 PM PST Hello, so I recently became interested in PayPal. The company has a solid user base (core service, Venmo), good growth opportunities (partnership with Amazon), and in general is undervalued right now (according to a lot of analyst opinions and where it is on its 52 week range.) I understand that it peaked during Covid but PayPal isn't primarily a "Covid business." Why is the stock price not recovering faster? Am I missing something? Is the PayPal stock price staying low an example of how social sentiment and momentum are becoming increasingly larger drivers of stock prices in favor of technicals? [link] [comments] | ||

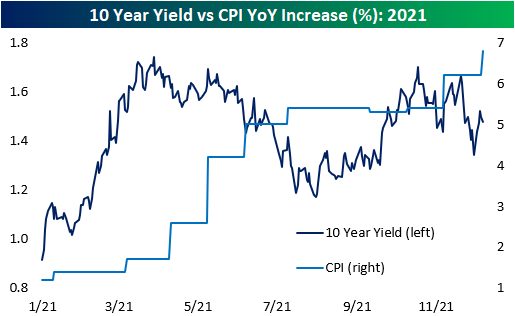

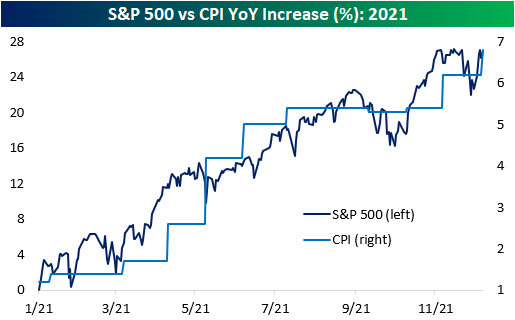

| Here is a Market Recap for today Friday, December 10, 2021. Please enjoy! Posted: 10 Dec 2021 02:37 PM PST PsychoMarket Recap - Friday, December 10, 2021 Stocks ended broadly higher today as market participants shrugged off the new Consumer Price Index (CPI), which is roughly in line with economist expectations ahead of the Federal Reserve final meeting of the year, a sign that market participants. The Russell 2000 (IWM) which tracks the performance of small-caps, underperformed today. Looking ahead, market participants wait for the Federal Reserve's final policy-setting meeting next week. Notable Numbers Today

The Labor Department released the Consumer Price Index, which showed the rate of inflation coming in at a multi-decade high for the month of November. CPI climbed 6.8% in a year-over-year period, marking the fastest rate of inflation since June 1982. Excluding volatile food and energy prices, the "core" CPI came in at 4.9%. On the other hand, new weekly unemployment claims in the US plunged to the lowest level since 1969, coming in even below pre-pandemic. Here are the numbers:

Currently, the US has more than 11 million job openings, highling how tight the labor market is becoming in the US. A tight labor market combined with elevated inflation will likely make the Federal Reserve to finish quantitative tapering sooner than expected. Seema Shah, Chief Investment Strategist at Principal Global Investors, said "Wage increases are probably on the agenda for next year. That's part of the broadening of inflationary pressures that we've already started to see come through in some of that CPI data. But I have to say that we're not so worried because we're starting to see other parts of the inflation picture actually starting to fade. So at the end of next year, 12 months from now, we're not expecting the kind of 6-7% CPI numbers ... We're thinking more like 3% level for 12 months time." Highlights

[link] [comments] | ||

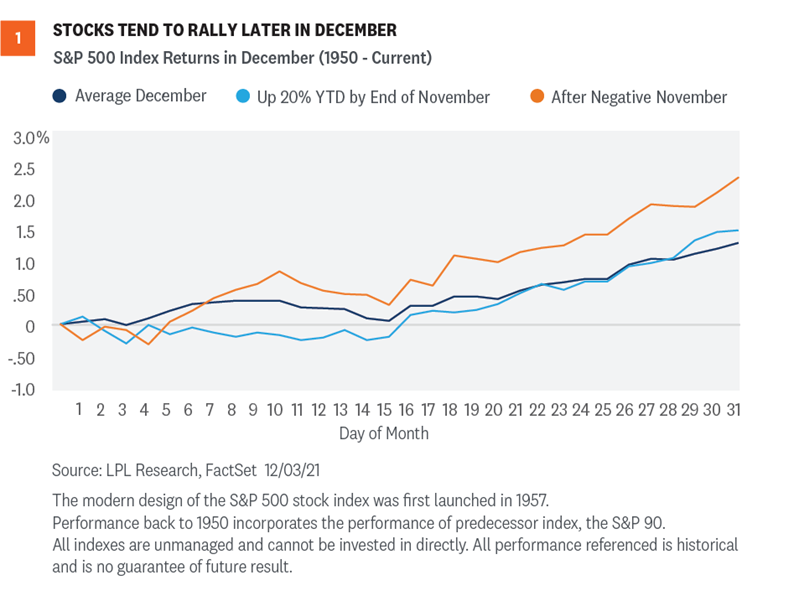

| Wall Street Week Ahead for the trading week beginning December 13th, 2021 Posted: 10 Dec 2021 05:07 PM PST Good Friday evening to all of you here on r/StockMarket. I hope everyone on this sub made out pretty nicely in the market this past week, and are ready for the new trading week ahead. Here is everything you need to know to get you ready for the trading week beginning December 13th, 2021. Fed is expected to speed up end of bond buying and signal interest rate hikes are coming - (Source)

This past week saw the following moves in the S&P:(CLICK HERE FOR THE FULL S&P TREE MAP FOR THE PAST WEEK!)S&P Sectors for this past week:(CLICK HERE FOR THE S&P SECTORS FOR THE PAST WEEK!)Major Indices for this past week:(CLICK HERE FOR THE MAJOR INDICES FOR THE PAST WEEK!)Major Futures Markets as of Friday's close:(CLICK HERE FOR THE MAJOR FUTURES INDICES AS OF FRIDAY!)Economic Calendar for the Week Ahead:(CLICK HERE FOR THE FULL ECONOMIC CALENDAR FOR THE WEEK AHEAD!)Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:(CLICK HERE FOR THE CHART!)S&P Sectors for the Past Week:(CLICK HERE FOR THE CHART!)Major Indices Pullback/Correction Levels as of Friday's close:(CLICK HERE FOR THE CHART!)Major Indices Rally Levels as of Friday's close:(CLICK HERE FOR THE CHART!)Most Anticipated Earnings Releases for this week:(CLICK HERE FOR THE CHART!)Here are the upcoming IPO's for this week:(CLICK HERE FOR THE CHART!)Friday's Stock Analyst Upgrades & Downgrades:(CLICK HERE FOR THE CHART LINK #1!)(CLICK HERE FOR THE CHART LINK #2!)(CLICK HERE FOR THE CHART LINK #3!)(CLICK HERE FOR THE CHART LINK #4!)(CLICK HERE FOR THE CHART LINK #5!)

STOCK MARKET VIDEO: Stock Market Analysis Video for Week Ending December 10th, 2021(CLICK HERE FOR THE YOUTUBE VIDEO!)STOCK MARKET VIDEO: ShadowTrader Video Weekly 12.12.21([CLICK HERE FOR THE YOUTUBE VIDEO!]())(VIDEO NOT YET POSTED.) Here are the most notable companies (tickers) reporting earnings in this upcoming trading week ahead-

(CLICK HERE FOR NEXT WEEK'S MOST NOTABLE EARNINGS RELEASES!)(CLICK HERE FOR NEXT WEEK'S HIGHEST VOLATILITY EARNINGS RELEASES!)Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

DISCUSS!What are you all watching for in this upcoming trading week? I hope you all have a wonderful weekend and a great trading week ahead r/StockMarket. :) [link] [comments] | ||

| Most Anticipated Earnings Releases for the trading week beginning December 13th, 2021 Posted: 10 Dec 2021 10:36 PM PST

| ||

| Posted: 10 Dec 2021 11:59 AM PST

| ||

| FRIDAY RUNDOWN: AMC, GME, ISIG, PPSI, CEI, VSTA Posted: 10 Dec 2021 09:05 PM PST

| ||

| Last 24 hours based on mentions in reddit. Posted: 10 Dec 2021 08:33 PM PST

| ||

| Posted: 09 Dec 2021 06:56 PM PST

| ||

| (12/10) Friday's Pre-Market Stock Movers & News Posted: 10 Dec 2021 05:02 AM PST Good Friday morning traders and investors of the r/StockMarket sub! Welcome to the final trading day of this week. Here are your pre-market movers & news this AM-Stock futures are positive ahead of key inflation report

STOCK FUTURES CURRENTLY:(CLICK HERE FOR STOCK FUTURES CHARTS!)YESTERDAY'S MARKET MAP:(CLICK HERE FOR YESTERDAY'S MARKET MAP!)TODAY'S MARKET MAP:(CLICK HERE FOR TODAY'S MARKET MAP!)YESTERDAY'S S&P SECTORS:(CLICK HERE FOR YESTERDAY'S S&P SECTORS CHART!)TODAY'S S&P SECTORS:(CLICK HERE FOR TODAY'S S&P SECTORS CHART!)TODAY'S ECONOMIC CALENDAR:(CLICK HERE FOR TODAY'S ECONOMIC CALENDAR!)NEXT WEEK'S ECONOMIC CALENDAR:(CLICK HERE FOR NEXT WEEK'S ECONOMIC CALENDAR!)NEXT WEEK'S UPCOMING IPO'S:(CLICK HERE FOR NEXT WEEK'S UPCOMING IPO'S!)NEXT WEEK'S EARNINGS CALENDAR:([CLICK HERE FOR NEXT WEEK'S EARNINGS CALENDAR!]())(T.B.A. THIS WEEKEND.) THIS MORNING'S PRE-MARKET EARNINGS CALENDAR:(N/A.) ([CLICK HERE FOR THIS MORNING'S EARNINGS CALENDAR!]())EARNINGS RELEASES BEFORE THE OPEN TODAY:(CLICK HERE FOR THIS MORNING'S EARNINGS RELEASES!)EARNINGS RELEASES AFTER THE CLOSE TODAY:([CLICK HERE FOR THIS AFTERNOON'S EARNINGS RELEASES!]())(NONE.) YESTERDAY'S ANALYST UPGRADES/DOWNGRADES:(CLICK HERE FOR YESTERDAY'S ANALYST UPGRADES/DOWNGRADES LINK #1!)(CLICK HERE FOR YESTERDAY'S ANALYST UPGRADES/DOWNGRADES LINK #2!)(CLICK HERE FOR YESTERDAY'S ANALYST UPGRADES/DOWNGRADES LINK #3!)YESTERDAY'S INSIDER TRADING FILINGS:(CLICK HERE FOR YESTERDAY'S INSIDER TRADING FILINGS!)TODAY'S DIVIDEND CALENDAR:(CLICK HERE FOR TODAY'S DIVIDEND CALENDAR LINK #1!)(CLICK HERE FOR TODAY'S DIVIDEND CALENDAR LINK #2!)(CLICK HERE FOR TODAY'S DIVIDEND CALENDAR LINK #3!)THIS MORNING'S MOST ACTIVE TRENDING TICKERS ON STOCKTWITS:

THIS MORNING'S STOCK NEWS MOVERS:(source: cnbc.com)

FULL DISCLOSURE:

DISCUSS!What's on everyone's radar for today's trading day ahead here at r/StockMarket? I hope you all have an excellent trading day ahead today on this Friday, December 10th, 2021! :)[link] [comments] | ||

| Morning Update for Friday, 12/10/21 Posted: 10 Dec 2021 05:47 AM PST Good morning everyone. Have a nice Friday, and enjoy your weekend :) This list is geared towards day trading. With the momentum watchlist especially, I am typically in and out very quickly, only occasionally longer than a couple minutes, usually faster scalps. Always have a plan when you enter a trade (for profit taking and for taking a loss), and use proper risk management for your account. Feel free to message me if you have any questions. Main Watchlist: Gapping UP:

Gapping DOWN:

Momentum Watchlist:

Market Outlook: Stocks are looking to open a bit higher after we saw some choppiness in the market yesterday. The major indices tested resistance levels before selling off, and I'll be watching those resistance levels closely in today's trading. The Labor Department is set to release the Consumer Price Index (CPI) for November, which is expected to show a climb of 6.8% over last year. This would be the highest rate since the 80's. We could see a shift in monetary policy from the Fed in early 2022 if inflation continues to rise like it is. SPY is trading just under 468. I'll be watching 469 and 470 as resistance levels this morning. If we fail to get back above these resistance levels we could see some more choppiness. If we see weakness, I'll watch 467 as potential support. DIA is trading a bit over 359. I'll be watching 360 as resistance. QQQ is trading just under 396. After rejecting 400 as resistance in yesterday's trading, I'll be watching that level today. If we see weakness, I'll be watching 394 as potential support. Gold and silver are each down a bit this morning. Crude oil is trading slightly higher, still holding above the $70 level. Bitcoin is trading around 49,900, seeing a nice bounce after yesterday's trading. It seems to still be finding support after the sell-off this past weekend. Ethereum is trading just over 4,200. After bouncing off the 4,000 support level earlier this morning, we could be due for some more upwards movement. Ethereum has been showing strength relative to Bitcoin lately, which is worth following. Crypto-related stocks are up in premarket trading as a result. Airlines and cruise stocks are somewhat mixed due to the uncertainty surrounding the omicron variant. Remember to use proper risk management, by making sure you size appropriately for your account and have a plan for every trade you enter (both for taking profits and cutting losses). Happy trading everyone :) [link] [comments] | ||

| The time to grab some GRAB is now Posted: 10 Dec 2021 11:55 AM PST This stock has over 50% short interest and has been climbing since coming public threw a SPAC on Dec 2. It is a Mega App in Asia, a tech Co that does it all. It is Uber, DoorDash, Paypal, Sofi, UPS, and more all in one. IT's does Transportation,Food Delivery, Grocery delivery,Parcel delivery, E-Commerce, Online Payments and Financial Services in Singapore, Malaysia, Thailand, Vietnam, Cambodia, Indonesia. Myanmar, and the Philippines. The stock is cut in half since its Listing on Dec 2. Its time to do a GAMESTOP on These MFing short hedges. This Co is Listed on Fortunes 50 Change The World List for addressing Social Issues during the Pandemic, It #2 on CNBC's Disruptor 50, This co helps the unbanked and underbanked by simplifying financial services in these in these countries. JP Morgan initiated coverage Dec 6 with an overweight rating. It is making a difference in these developing countries [link] [comments] | ||

| The US government is asking Tesla why it lets people play video games while driving Posted: 09 Dec 2021 11:33 PM PST

| ||

| Tesla Under Fire For Allowing Drivers To Play Games While Driving Posted: 09 Dec 2021 04:07 PM PST |

![[link]](https://i.redd.it/9q234nru0p481.jpg){kind=link}

![[link]](https://i.imgur.com/iZZ19j3.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[link]](https://i.redd.it/qluh9589zu481.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| You are subscribed to email updates from r/StockMarket - Reddit's Front Page of the Stock Market. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment