Financial Independence Weekly “Help Me FIRE!” thread. Post your detailed information for highly specific advice - July 05, 2021 |

- Weekly “Help Me FIRE!” thread. Post your detailed information for highly specific advice - July 05, 2021

- Daily FI discussion thread - Monday, July 05, 2021

- FIRE in one of the most expensive countries in the world as a 25yo couple.

- Weekly FI Monday Milestone thread - July 05, 2021

| Posted: 05 Jul 2021 02:01 AM PDT Need help applying broader FIRE principles to your own situation? We're here for you! Post your detailed personal "case study" and ask as many questions as you like, or help others who've done the same. Not sure if your questions pertain? Post them anyway…you might be surprised. It'll be helpful to use our suggested format. Simply copy/paste/fill in/etc. But since everybody's situation is different, feel free to tailor your layout to your needs. -Introduce yourself -Age / Industry / Location -General goals -Target FIRE Age / Amount / Withdrawal Rate / Location -Educational background and plans -Career situation and plans -Current and future income breakdown, including one-time events -Budget breakdown -Asset breakdown, including home, cars, etc. -Debt breakdown -Health concerns -Family: current situation / future plans / special needs / elderly parents -Other info -Questions? [link] [comments] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Daily FI discussion thread - Monday, July 05, 2021 Posted: 05 Jul 2021 02:00 AM PDT Please use this thread to have discussions which you don't feel warrant a new post to the sub. While the Rules for posting questions on the basics of personal finance/investing topics are relaxed a little bit here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Have a look at the FAQ for this subreddit before posting to see if your question is frequently asked. Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

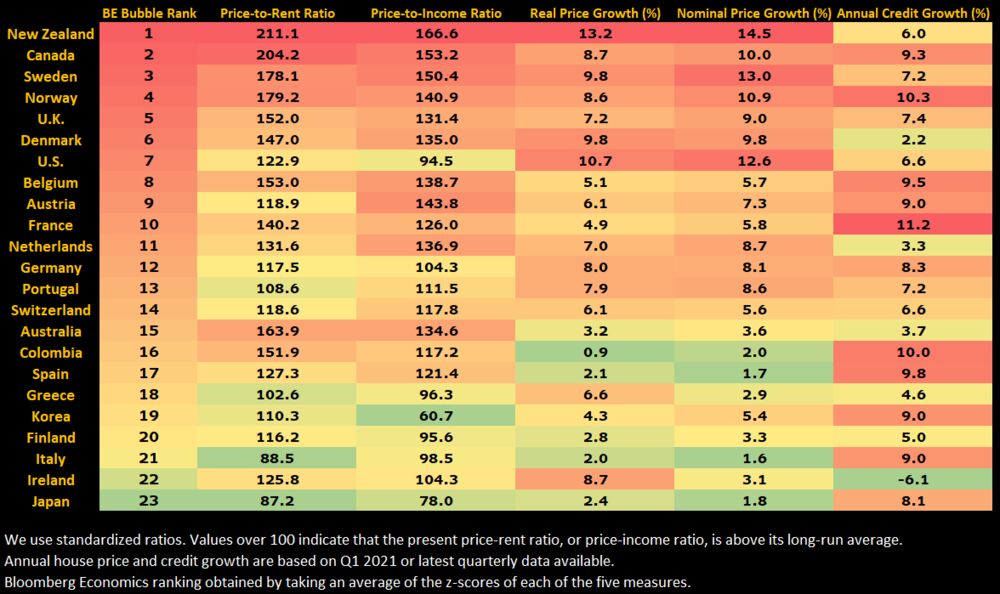

| FIRE in one of the most expensive countries in the world as a 25yo couple. Posted: 05 Jul 2021 01:14 PM PDT EDIT: Thank you for the comments - I think I have likely overstated the cost of living here compared to other countries. My points around housing stand, but it seems that NZ is closer to US/Europe in general cost of goods/services than I previously thought! I feel that on a median basis a New Zealander may not be far off an American or European standard and cost of living. One big difference being that Kiwis can't really move to a LCOL area as easily as Americans can. We don't have a Midwest, or cheaper souther states to do "geographical arbitrage" like some people talk about in this sub. Income trajectory is also worse here in my opinion. The median wage for the US will include many millions of people who live in these LCOL States, for which there is little equivalent here. Thanks again for the feedback - I have learned a lot :) Cost of living in New Zealand First I'd like to paint a bit of a picture of the cost of living in our country. In addition to generally expensive goods, we are in the midst of the largest housing "bubble" in the world. Housing is widely considered to be a national crisis, and due to long running net immigration into New Zealand, there are some big question marks over what might happen when the borders re-open. With some bold predictions (article about house prices doubling in 5 years). Past and present governments have been ineffective at moderating our rapidly increasing house and rent prices. Taxes are also high compared to the US (I think?). I am currently paying an effective tax rate of 27%. Here is a table of some common items and their cost. I haven't picked these to show any particular disparity with the US or other countries, but I thought they might highlight some interesting differences. For reference, the average annual household income in New Zealand is $107,000 ($75,000 USD). I believe this is more than the US average, but this difference would almost certainly be closed due to the astronomical cost of living here.

Here is a picture that can hopefully put our insane housing situation into perspective. I should also point out some of the financial pros of living here. Medical costs are significantly lower than in the US. Reading posts on this subreddit about people who have achieved FIRE but continue working solely for the medical insurance boggles my mind. We pay around $215 a month for private health insurance – which we don't even necessarily need. One of us recently had surgery at a private hospital that would have cost $35,000. This was completely paid for by the government – irrespective of our insurance situation. We both have degrees and student loans. Our loans are interest free for the life of the loan. If we move overseas then we will have to pay interest (at 4% I believe). Loan repayments are automatically garnished from your wages, after an initial repayment free threshold of ~$20k a year. The government provides a living cost supplement to students at university – to be repaid. Those who can demonstrate a low enough household income (parents) can receive a non-repayable student allowance of $240 a week. This system is flawed however, as it assumes that parents over a certain income threshold are helping their children financially through university – which is not always the case. Our situation: I grew up in a single parent household with two other siblings. My mother was incredibly disciplined with money – keeping handwritten budgets and tracking expenditure religiously. This was out of necessity, but I believe it laid the groundwork for my relationship with money. From a very young age I recall wanting to be wealthy when I was older. Mostly from the point of view of having stability and security over my life situation. I had a head for numbers and had various "side hustles" throughout my youth – at one point bulk buying Mentos and re-selling them at school. I was lucky enough to stumble into the FIRE movement very early. I cannot remember the exact age when I came across "that" Mr Money Moustache article, but I may have been 20 at the time. I was saving and investing throughout university of my own volition but with no particular goal in mind. The concepts of FIRE appealed to me immediately, and I switched focus to trying to GTFO of the workforce ASAP. My partner grew up the youngest of 5 siblings. Money was tight in the house – homemade food was common, taking advantage of what was grown in the garden or purchased in bulk and frozen for later. Her father was self-employed which meant a variable household income. During university she was working up to five jobs at a time, so that sets a picture of the sort of work ethic she has. Work History: We both started our careers as graduates at consulting firm working in the Risk Management area. After a couple of years, we both moved to the same company. A short time later we moved jobs again, after which I moved once more to where I am now. I am a firm believer in frequent career moves to accelerate your earning potential. The below chart reflects this. I would say that we are on very good money for our age. New Zealand certainly has a lower ceiling on earnings compared to the US. Making $100k USD would be rare, although we are lucky enough to potentially hit that number soon. Some of the figures you see on this sub (e.g. $250k USD) are almost unattainable here, perhaps outside of specialised medical personnel, C-suite execs, and partners at law firms, etc. But we all know that FIRE attracts a lot of confirmation bias and high tech salaries.

Our Housing bubble ride: We were incredibly lucky to purchase our first home in 2019 for $690k ($484k USD). It is a 100sqm (1076 square foot) three-bedroom house. Most young people in New Zealand have dwindling hopes of ever owning their own home. For an individual on the median wage, rent will absorb a significant percentage of income, to the point where saving for a deposit on a house is nearly impossible. The current climate is that only well-paid couples, those with significant help from parents, or very high income individuals are capable of purchasing a home. We fell into the first bucket, and benefited from years of savings even at a young age at the time of purchase. This is the reality of our current housing market that you essentially have to be frugal and a high earner from the second you hit adulthood if you want a hope of owning, and even that will likely not be enough as prices continue to soar. In less than two years the current value of our property is $950k ($667k USD). We have purchased a second home that is yet to be built, and we intend to sell our current property when we move. We have no intention of being landlords or property investors, as this simply feeds into the current crisis. The proceeds from this sale will be put into index funds, as well as financing the new house. Other investments: We follow the usual strategy of investing in low-cost diversified index funds. Mostly VOO. Lifestyle: We are generally very frugal. My partner budgets but I do not. Despite food being very expensive here, our weekly spend for groceries is about $140 ($97 USD). This is quite low compared to other people I have asked. We do not eat out; we make our own lunches for work and always have done. I think I can count on two hands the number of times I have purchased lunch since I started working in 2017. We own one car which is paid in full, although we are upgrading to a brand-new car later in the year to take advantage of a government subsidy for electric vehicles and hybrids (we will get $5750 back). I would consider this to be one of the first intentionally not-great financial decisions we've made. But we are in a spot where we can afford it, and it is part of planning for our future. Hobbies are relatively low cost and high repeatability – things like gaming, yoga, running, gardening, reading, hiking. We travel domestically quite a bit, particularly for road trips and hiking. COVID has obviously put a halt on any international travel. The future: One unique aspect of FIRE in New Zealand is the prospect of having a freehold home. It is entirely feasible that we could have ~$2mil NW but still be paying a significant mortgage. One potential solution will be to move to a cheaper area of the country (there aren't many) and try to go no-debt. We plan to continue building our index investments. I am particularly keen on holding VOO, or other international investments, as it acts as an inflation hedge in a worst-case scenario if the NZ economy continues on its current path. Many young Kiwis are looking overseas for better earning prospects. A common path is for young people to move overseas to advance their careers and savings, and to then come back and buy a home. We plan to travel, and possibly work in another country, but we are in a good spot in terms of earnings so this is not as much of a priority for us. As property owners, we are likely to see continued growth in our home(s) value. Our current equity forms a significant portion of our net worth, and is part of the reason for wanting to sell in order to lock in the "gains" and diversify. In New Zealand we have been talking about "when the bubble pops" since the 90s, and at this point it seems inevitable that house prices will continue to increase. We are the perfect storm of a small country with limited land but huge immigration demand due to our perception on the world stage. Not to mention the historic underinvestment and poor planning by government and city councils around good property development practices. Our generation is feeling the pinch, and we are part of the lucky few who will benefit from this continued crisis. The figures: I have been tracking my net worth for exactly 6 years. My partner for ~2 years (we are the same age).

Looking at these figures it becomes clear that the bull market (both shares and housing) of 2020 has had an enormous impact on our net worth. We did well off some stock picks during the COVID market recovery, but now it's back to nothing but VOO. The house price growth in particular is practically a windfall in terms of size and its sudden appearance. My hope is that once this is reinvested into index funds that it serves as the foundation of more sustainable portfolio growth for the future. The common saying around these parts is that the first $100k is the hardest, and I still can't wrap my head around the fact that we essentially blew through the first $100k and into $400k+ in a single year. I also feel that these numbers downplay our savings efforts in some way. My early net worth fluctuation was due to being over-invested in a small number of highly volatile companies, and the figure was weighed down by $40k+ in student loan debt. Combined we have paid down more than $50k in student loan debt already. Although I have not tracked it, I have likely averaged a 40% savings rate at a minimum. I think that even without the house purchase and subsequent price rise, we would be in a pretty admirable position – although those USD figures don't look as impressive… To conclude: I suppose the purpose of this post is to provide some insight into what FIRE can look like outside of US/Europe, and also to talk about our insane housing market. If we were doing comparable jobs in the US I believe our journey to FI would be substantially shorter, but despite the cost of living (and in fact due to our privilege of being able to pursue FIRE in such a HCOL country) we are very happy to be where we are. Maybe this post can give some info for all of those hopeful immigrants who think NZ is simply the land of milk and honey! We do have a lot to be grateful for here, but financially it can be a tough situtaion for many people. [link] [comments] | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Weekly FI Monday Milestone thread - July 05, 2021 Posted: 05 Jul 2021 02:00 AM PDT Please use this thread to post your milestones, humblebrags and status updates which you don't feel warrant a new post to the sub. While the Rules for posting questions on the basics of personal finance/investing topics are relaxed a little bit here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] |

{kind=link}

| You are subscribed to email updates from Financial Independence / Retire Early. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment