Daily General Discussion and spitballin thread Investing |

- Daily General Discussion and spitballin thread

- Daily Advice Thread - All basic help or advice questions must be posted here.

- Spotify removes hundreds of K-pop songs globally, unable to reach an agreement with Kakao M

- MMED/MMEDF - long term 10+ bagger

- Rocket Lab is going public on a SPAC at a $4.1 billion valuation and unveils a new rocket

- KMPH Got FDA Approval tonight!

- Wall Street ends lower as Apple and Tesla retreat

- Warren Buffett Says Berkshire's Apple Investment Shows The 'Power Of Repurchases'

- Commas after Commodity Futures Quotes

- Fastly (FSLY) Full Due Diligence Post - Promising Company at Relatively Fair Valuation

- Mining for car batteries . Study in link

- $BUZZ ETF - Barstool’s Dave Portnoy promotes new fund

- China is sounding the alarm about a global market bubble

- High Times IPO - A Dying Brand —> From Selling Mags to Selling Bags

- The Case for $RILY: A Financial Sector Sleeper DD

- investing in non-registered assets

- $EBON - Crypto Miner, Mining Equipment Seller, ASIC maker and EBONEX Crypto Exchange

- Electric Jet-Ski and Snowmobile maker Taiga Motors to go public in merger via Canaccord SPAC CGGZ

- Silver DD Article - Potential rise to $50

| Daily General Discussion and spitballin thread Posted: 03 Mar 2021 02:01 AM PST Have a general question? Want to offer some commentary on markets? Maybe you would just like to throw out a neat fact that doesn't warrant a self post? Feel free to post here! This thread is for:

Keep in mind that this subreddit, and this thread, is not an appropriate venue for questions that should be directed towards your broker's customer support or google. If you would like to ask a question about your personal situation or if you are asking for advice please keep these posts in the daily advice thread as that thread is more well suited for those questions. Any posts that should be comments in this thread will likely be removed. [link] [comments] |

| Daily Advice Thread - All basic help or advice questions must be posted here. Posted: 03 Mar 2021 02:00 AM PST If your question is "I have $10,000, what do I do?" or other "advice for my personal situation" questions, you should include relevant information, such as the following:

Please consider consulting our FAQ first - https://www.reddit.com/r/investing/wiki/faq And our side bar also has useful resources. Be aware that these answers are just opinions of Redditors and should be used as a starting point for your research. You should strongly consider seeing a registered financial rep before making any financial decisions! [link] [comments] |

| Spotify removes hundreds of K-pop songs globally, unable to reach an agreement with Kakao M Posted: 02 Mar 2021 06:01 AM PST Original article: https://www.nme.com/news/music/hundreds-k-pop-releases-removed-spotify-worldwide-2890528

Kakao M claiming it was Spotify removing it:

While this is clearly over compensation, Spotify needs to rectify this asap. From their own news release, K-pop is a huge part of why people use their service:

If a resolution can't be reached I think Spotify will be in trouble long-term as whatever service picks it up will siphon a significant chunk of users. [link] [comments] |

| MMED/MMEDF - long term 10+ bagger Posted: 02 Mar 2021 09:41 PM PST Hello everyone. Not sure how many people are familiar with the psychedelic space, but I'm here to tell you guys a bit about mindmed and the space as a whole. The basic investment thesis is this: current available mental health treatments such as adderall, Xanax, suboxone, etc simply dull out, or put a temporary bandaid on the issue. After looking at the efficacy rates for issues such as smoking cessation, PTSD, treatment resistant depression, etc, it is clear that psychedelics could turn into a massive industry that disrupts the way we treat mental health. This could lead mind medicine and other similar companies to multi billion dollar buyouts from big pharma companies. There are plenty of fantastic companies in the space, but mindmed is by far my favourite. For full disclosure I'm currently long ~100k warrants, already up bigly. Mindmed has a diverse pipeline for a multitude of issues, plenty of cash for future R&D, and plenty of fantastic partnerships in academia/pharma. Additionally, this stock cannot be traded yet by anyone on robinhood due to it being on the OTC market. A nasdaq uplist (expected) would open the floodgates to a ton of new retail buyers. There is also EXTREMELY low institutional ownership, basically 0%. At a market cap of 1.5 billion Canadian dollars, this can easily be a 10 bagger once there is more media attention surrounding it, and more progress is made regarding clinical trials. People are not talking about the psychedelic space yet. Last thing before I start seeing this in the comments, this does NOT at all compare to the weed industry. There are far more barriers to entry, addresses a totally different market (recreational vs medicinal), and has the added advantage of interest from big pharma. I'm aware this isn't very detailed or anything, I don't have the patience to put together a full DD post. I'm simply encouraging everyone in this group to do consider what this company has going for it. [link] [comments] |

| Rocket Lab is going public on a SPAC at a $4.1 billion valuation and unveils a new rocket Posted: 02 Mar 2021 12:07 PM PST Rocket Lab, a developer of launch vehicles and smallsats, will merge with a special-purpose acquisition company (SPAC) to support development of a larger launch vehicle, part of the latest wave of deals to take space companies public. The SPAC deal values Rocket Lab at $4.1 billion and is expected to close in the second quarter of 2021. Once the merger is done, Vector Acquisition Corporation, the SPAC Rocket Lab is merging with, will change its name to Rocket Lab USA, Inc, and the Nasdaq ticker symbol will be RKLB. The merger will provide Rocket Lab with up to $320 million from Vector Acquisition's account. In addition, a concurrent private investment in public equity (PIPE) round, led by Vector Capital, BlackRock and Neuberger Berman, will provide $470 million. The company will have $750 million in cash when the deal closes, fueling development of the company's next rocket dubbed Neutron, a fully reusable launch vehicle capable of lifting eight tons to orbit. The rocket is "tailored for mega constellations, deep space missions and human spaceflight," the company said in a statement. [link] [comments] |

| KMPH Got FDA Approval tonight! Posted: 02 Mar 2021 09:37 PM PST Yes!!! I've been in this since .19 a share. Closed at 9.91 today and finally got FDA approval. The stock ripped all the Band-Aids off before getting approval. It has zero debt, cash in hand, low cash burn, 50 million dollar milestone payment hitting with labeling. Short squeeze coming from all the shorts that bet wrong. "KemPharm may be eligible for up to $468 million in regulatory and sales milestone payments, as well as tiered royalty payments, on a product-by-product basis for net sales, with potential percentages up to the mid-twenties for U.S. net sales, and up to the mid-single digits of net sales in each country outside of the U.S." [link] [comments] |

| Wall Street ends lower as Apple and Tesla retreat Posted: 02 Mar 2021 02:12 PM PST (Reuters) - Wall Street ended lower on Tuesday, pulled down by Apple (NASDAQ:AAPL) and Tesla (NASDAQ:TSLA), while materials stocks climbed as investors waited for the U.S. Congress to approve another stimulus package. Following strong gains in the prior session, technology shares dipped in the resumption of a rotation by investors out of stocks that outperformed due to the coronavirus pandemic and into others viewed as likely to do well as the economy recovers. The S&P 500 materials and consumer staples sector indexes rose. [link] [comments] |

| Warren Buffett Says Berkshire's Apple Investment Shows The 'Power Of Repurchases' Posted: 02 Mar 2021 06:58 AM PST Berkshire Hathaway Inc (NYSE: BRK-A) (NYSE: BRK-B) CEO Warren Buffett over the weekend wrote his annual letter to shareholders and highlighted the "power of repurchases" using Apple Inc (NASDAQ: AAPL) as an example. What Happened: Buffett said that Berkshire began buying shares of the iPhone maker in late 2016 and by early June 2018 owned more than one billion shares (adjusted for splits). "Saying that, I'm referencing the investment held in Berkshire's general account and am excluding a very small and separately-managed holding of Apple shares that was subsequently sold. When we finished our purchases in mid-2018, Berkshire's general account owned 5.2% of Apple," wrote the veteran investor. The cost for acquiring that stake was $36 billion and since then Berkshire has enjoyed regular dividends averaging about $775 million annually and has pocketed an extra $11 billion in 2020 by selling a small part of its holdings. The continuous repurchase of shares by Apple and the consequent shrinking number of shares outstanding has meant that Berkshire now owns 5.4% of the Tim Cook-led company. "That increase was costless to us," wrote Buffett. Why It Matters: Berkshire's third-quarter operating profits declined 32% to $5.48 billion from $8.07 billion a year ago. The company repurchased .3 billion worth of stock in the period. Since Berkshire also repurchased its own shares during the past two and a half years, its shareholders now own a full 10% more of Apple's assets and future earnings than they did in July 2018, wrote Buffett. "This agreeable dynamic continues. Berkshire has repurchased more shares since yearend and is likely to further reduce its share count in the future," revealed the Oracle of Omaha. Buffett also pointed to Apple's publicly stated intention to repurchase shares and thus Berkshire shareholders would find "their indirect ownership of Apple increasing as well." This year the Buffet-led company cut its position in Apple by 6% to 887 million shares in the latest quarter but upped stakes in AbbVie Inc (NYSE: ABBV), Bristol-Myers Squibb Company (NYSE: BMY), and Merck & Co, Inc (NYSE: MRK). Apple still remains the single largest investment in Berkshire's portfolio. Price Action: Berkshire Class A shares closed nearly 0.9% lower at $364,580 on Friday. On the same day, the company's Class B shares closed 1.3% lower at $240.51. Apple shares closed almost 0.2% higher at $121.26 and fell 0.41% in the after-hours session. Shivdeep Dhaliwal Mon, March 1, 2021, 1:28 AM·2 min read [link] [comments] |

| Commas after Commodity Futures Quotes Posted: 03 Mar 2021 03:36 AM PST I'm working on a project that involves taking commodity futures quotes from the CME website, but I stumbled upon a weird thing. Some commodities are quoted using ' as a decimal separator. For example, May 21 Corn futures are currently 538'6 on the CME website (link). The number after the apostrophe is always a 0, 2, 4 or 6. I have never seen this format before, and even though I searched in many places, I can't find an explanation. Does anyone know how I can "translate" quotes like 1410'4 to USD? I'm pretty sure I can't just swap the ' for a comma. If you want to, you can access the specific report that I'm working with using this link Thanks for the help. [link] [comments] |

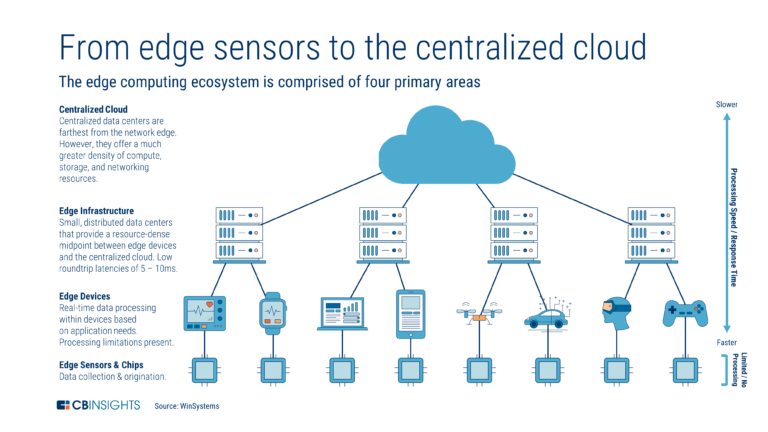

| Fastly (FSLY) Full Due Diligence Post - Promising Company at Relatively Fair Valuation Posted: 02 Mar 2021 08:21 AM PST Hello! Below is some diligence on Fastly, one of the innovators of the CDN / edge computing space. TDLR and resources used at the bottom. What are CDNs and Edge Computing?

The History of Fastly

Fastly's Products

Competitive Positioning

Customers

Financial Overview

Resources Used

TLDR: Fastly is a leader in the CDN and edge computing space with 2 innovative products (Compute@Edge and Secure@Edge) that could be strong growth drivers for years to come (given strong execution). The company is boasting strong growth and has been a victim of its own success but is trading at relatively reasonably multiples for a leading software company. [link] [comments] |

| Mining for car batteries . Study in link Posted: 02 Mar 2021 12:36 PM PST These are the mining stocks in Lithium + copper + nickel + cobalt + manganese + rare earth + silver. I have REEMF + REZZF + ABML + AMYZYF + ALYI + TLOFF + ILHMF + SXOOF + UAMY + FCSMF + MLLOF + HNCKF + COCBF + BMIX A new study did a deep dive into the emissions from the full life cycles, from petroleum extraction to mining, of both electric cars and fossil fuel-powered cars. The result is unsurprising but needed to dispel misinformation. One of the oil industry's favorite ways to try to attack electric cars was to say that they are just as polluting as gas-powered vehicles because they were powered by an electric grid that burns coal and natural gas. That has already been disproved by several studies, and the advantage for electric vehicles is growing as the grid is becoming cleaner with a higher mix of solar, wind, and hydropower in most markets. Now the oil industry is using another argument to discredit electric vehicles: mining resources to build batteries is just as bad as the environment as burning petrol. Like the argument about the grid, we thought that it was flawed due to battery recycling and now a study confirms it. Transport and Environment (T&E), an NGO that looks into the impact of transport on the environment, has released a new study that looks to compare emissions from raw materials to produce electric cars versus gas-powered vehicles: vehicles: "T&E's study assesses the amount of raw materials needed to make electric vehicle batteries today and in the future – taking into account changes in manufacturing processes and recycling. It compares this with the raw materials needed to run a fossil fuel car to show that electric car batteries need significantly less raw materials." The study focuses on some of the aspects that are often missed in emissions from full life cycles of gas versus electric. For the electric vehicles, it's the fact that you don't just burn a battery pack like you burn gas. T&E found that only about 30 kilograms of metals would be lost after recycling in an electric car battery pack. In comparison, an average gas-powered car will burn 300 to 400 times that weight in gas over its lifetime. The study also highlights that petrol extraction and refining are also extremely energy extensive parts of the oil industry that often relies on the same grid as electric vehicles do for charging. Here are the key findings from the study: Electric vehicles consume far less raw material (metals) than fossil fueled cars When taking into account the recycling of the battery cell materials and that the majority of the metal content is recovered, T&E calculates how much is 'consumed' or 'lost' during the lifetime of an EV. Under the EU's current recycling recovery rate target, around 30 kilograms of metals would be lost (i.e. not recovered). In contrast, the study shows that the weight of petrol or diesel that is burned during the average lifetime of a vehicle is around 300-400 times more than the total quantity of battery cells metals 'lost'. Over its lifetime, an average ICE car burns close to 17,000 liters of petrol, which would be equivalent to a stack of oil barrels 90m high. Less raw material will be needed for batteries over time Technological advancements will drive down the amount of lithium required to make an EV battery by half over the next decade. The amount of cobalt required will drop by more than three-quarters and nickel by around a fifth. Europe will need to import less raw material because of recycling In 2035 over a fifth of the lithium and nickel, and 65% of the cobalt, needed to make a new battery could come from recycling. Europe will likely produce enough batteries to supply its own EV market as early as 2021 T&E calculates that there will be 460 GWh (in 2025) and 700 GWh (2030) of battery production in Europe – enough to meet the demand of electric cars. Here's the study in full: [link] [comments] |

| $BUZZ ETF - Barstool’s Dave Portnoy promotes new fund Posted: 02 Mar 2021 11:05 AM PST On Thursday March 4th, $BUZZ, an ETF that tracks the top 75 large-cap stocks with social media attention, will launch on the NYSE. The algorithm that $BUZZ uses has been around for 5 years and claims to have outperformed the S&P 500 last year by 40%. The algorithm is based off of stocks with the most "buzz" and conversation on social media (not sure exactly which platforms) that also meet the criteria of being a large-cap stock. Dave Portnoy's involvement, despite his controversies, ultimately leads to more buzz for $BUZZ itself, thanks to $PENN, DDTG, and his many public appearances on CNBC, CNN, Fox News, etc. He may be used mainly as a promotion tool. [link] [comments] |

| China is sounding the alarm about a global market bubble Posted: 02 Mar 2021 07:55 AM PST https://edition.cnn.com/2021/03/02/investing/china-banking-financial-bubble-intl-hnk/index.html

[link] [comments] |

| High Times IPO - A Dying Brand —> From Selling Mags to Selling Bags Posted: 02 Mar 2021 09:09 PM PST High Times is a - beloved - American monthly magazine and cannabis brand with offices in Los Angeles and New York City. The magazine was founded in 1974 by Tom Forçade and the publication advocates the legalization of cannabis. The magazine has been involved in the marijuana-using counterculture since its inception. On Jan 29th, 2020, ditched dreams of NASDAQ Listing

High Times securities lawyers, Stephen Weiss and Megan Penick of L.A. based Michelman Robinson LLP, confirmed in an email interview that the company can not accept sales until they get their annual report filed and publicly available for investors. High Times IPO - Sorry, No Refunds - Teri Buhl of Cannabis Law Reports Talks Reg A Harvest Acquisitions It was in March that Harvest Health announced an $80 million buyout of that entire company. Then, literally two months later, we see a letter of intent filed by Hightimes now and Harvest saying,

Why that was contradictory is that Harvest had just been on an investor call telling people, when an analyst asked,

It didn't make sense that two months later they're getting rid of everything they just bought in California. Additionally, in the last month there have beenmultiple news reports questioning if Harvest even has ownership or control of the cannabis licenses to sell to High Times. Very little cash actually changes hands in the deals crafted by High Times; instead it has announced millions of stock (which isn't publicly traded yet) will pay for the asset purchases. With the Harvest acquisition, High Times attorney Stephen Weiss confirmed for CLR that $1.5 million was paid to Harvest but at signing only $500k was given. The asset purchase agreement filed with the SEC said High Times would pay Harvest $1 million on signing. This is just a complete lack of transparency, and it's completely unfair for the Main Street investor trying to get into cannabis. Done before starting The Securities and Exchange Commission has told a U.S. operated cannabis media and dispensary company, High Times Holdings, that they must halt accepting investments in their mini-IPO because they have failed to meet an extended deadline to file their audited annual report.

High Times used a reporting extension the SEC created because of the Covid-19 pandemic to get a 45 day extension to file the annual report and said in recent SEC disclosure filings, called Form 1-U, that they promised investors to get them current revenue, cash flows, debt levels and asset values by June 12, 2020 via the annual report; but CLR has learnt that this never happened. Adam Levin's company has spent over two years trying to get main street to invest up to $US50 million without a successful close date that could lead to publicly traded stock on the OTC Markets under the ticker $HITM. On June 30th, 2020 the company made an SEC filing announcing once again their mini-ipo would be extended for yet another three months but left out the important fact that they couldn't actually accept sales. When asked if it is normal practice for a Reg A issuer to continue to solicit investments when it can't accept sales; securities attorney Sara Hanks said: "The SEC may have softened up in the Covid crisis but previously, both sales and offers were supposed to stop during such time as the issuer was delinquent in its filings, because there is no exemption under Reg A for "offers" (advertising etc) while a company is delinquent." High Times still has their investment offering page live Since then investors have seen a rapid pace of public announcements about asset purchases, via signed letter of intents, hyping the potential growth of High Times followed up with quiet SEC filings announcing the deals had either fallen apart or been watered down. I have personally fallen for this sham (F), as I invested in 5000 units in 2018. They stopped responding to my inquires, in fact, there was a random charge on my credit card (from an airport in LA) the same day they charged my card for the IPO.. they stated that it would be refunded - never was. I can still log on and see the shares I have "invested" but they obviosuly don't represent anything. Lesson learned.. Recent Financials The company filed apost-qualification amendment to its Form 1-A with the SEC that suggests the financial condition has become even more precarious. In the first quarter of 2018, sales plunged 64.9% to just $1.481 million: Most of the decline can be attributed to the events business, which fell almost 83%, but publishing revenue declined over 16% as well. The company indicated that its Cannabis Cup events will take place later in the year compared to the prior year, with one in Las Vegas and in Los Angeles taking place in the first quarter of 2017 and none in the first quarter of 2018. The $554K in sales were generated by smaller events, and the company expects the number of Cannabis Cups and small events to increase for the full year. It blamed the publishing decline on lower sales at the newsstands and through subscription and lower print advertising revenue, with digital partially offsetting these factors. The company provided information about its cost of revenue, which was $503K, as well as its operating expenses, which declined substantially to $2.391 million, producing an operating loss of $1.413 million compared to an operating loss in the first quarter of 2017 of $6.54 million. Much of the year-ago operating expenses were due to a one-time non-cash charge of $6.689 million for equity compensation charges for consulting. The last time the company filed official annual earnings was June 2019. High Times had told investors it would get updated financial information on June 12, but that did not happen. The company has extended the offering of shares for two years, initially telling investors that it would list its shares on the NASDAQ. Then it lowered those expectations to the Over-The-Counter Marketplace. Still, it hasn't happened. I am not a Financial Advisor, so please do your own DD [link] [comments] |

| The Case for $RILY: A Financial Sector Sleeper DD Posted: 02 Mar 2021 01:44 PM PST This is my first attempt at a DD, so bear with me as I go through this.

BACKGROUND The company I'm looking at today is B Riley Financial (Nasdaq:$RILY). The company is a broad financial services provider which started as an investment bank and currently includes segments in capital markets, auction and liquidation, valuation and appraisal, and principal investments.

The capital markets segment provides an array of investment banking, corporate finance, research, wealth management, sales and trading services to corporate, institutional and high net worth clients.

The auction and liquidation segment utilizes a network of independent contractors and industry-specific advisors to tailor its services to the needs of a multitude of clients, logistical challenges and distressed circumstances.

The valuation and appraisal segment provides valuation and appraisal services to financial institutions, lenders, private equity firms and other providers of capital.

The principal investments consists of businesses which have been acquired primarily for attractive investment return characteristics.

FINANCIALS RILY recenly released their Q4 2020 and FY2020 results last week of which the following are highlghts:

Fourth Quarter 2020 Financial Highlights

Full Year 2020 Financial Highlights

Additionally, with the earnings release, they announced an increase to their quarterly dividend from $0.35 per share to $0.50 per share as well as a special dividend of $3.00 per share for a total dividend to stockholders of record on or around March 24th of $3.50 per share. This would bring the dividend to about a roughly 5.4% rate which is a very strong return (looking at you $RKT folks)

OUTSIDE RESEARCH AND HISTORY So how has the company done over time you ask? Since 2016 revenue has grown from $190 million in to an estimated $798 million in 2020, a ~42% CAGR. EBITDA has grown from $48.9 million to approximately $406 million or a ~65% CAGR, and the regular dividend has grown from $0.32 to $1.50. Additionally, they recently completed the acquisition of National Holdings Corporation, another wealth management firm, with asset management of approximately $20 billion to add to the already existing $12 billion management portfolio. Since this is a recent acquisition income and revenue from this acquisition won't hit the financials until the Q1 earnings are released at the earliest.

Additionally, just yesterday they announced the full redemption of 7.5% Senior Notes due in 2027 showing another strong financial indicator. Also, the largeest shareholder in the company, CEO Bryant Riley, has continued to be bullish in his own company with continued stock buy backs through out the last few years, with the most recent being a $4.6 MM purchase in January at $46 a share. A lot of conviction in the long term growth in the company from the C-Suite folks.

Lastly, I'll leave this bit of research from hype machine Seeking Alpha, which notes that RILY is trading at a deep discount in relation to it's peers is the financial sector. It currently trades roughly around 3x to 4x EBITDA, while other firms in the sector are trading around 14x. Now, this isn't to say that RILY will be at that 14x rate, but it does lend some credence to where it could go. Seeking Alpha goes on to note that even at a 40% discount from it's 14x EBITDA would put the price per share around $111, which would represent a 71% increase in value from the current stock price.

CONCLUSION I feel as those this might be a hidden gem in the financial sector as it has a very diversified set of offerings that can benefit from both up and down markets. Additionally, leadership has show strong conviction in the company and analyst feel as those the long term gains are there. I don't know if $111 or $150 a share is on the horizon, but I'll be very interested to find out and see where this one goes. [link] [comments] |

| investing in non-registered assets Posted: 02 Mar 2021 10:03 PM PST Does anyone have any experience (good or bad or other) investing in non traditional, non-registered assets? Aside from physical gold and silver and a few graded dual lands (expensive trading cards) I haven't really gotten into the space. I obviously would not have a large percentage of my portfolio in this kind of thing since it's a pain to liquidate, but I do like the idea of having fun investments and parking money in some weird assets - especially if inflation rates skyrocket down the road. I've taken a look at prices of high end collectibles, wines, cigars, art, etc and they all seem to beat the S&P over time. Any thoughts? [link] [comments] |

| $EBON - Crypto Miner, Mining Equipment Seller, ASIC maker and EBONEX Crypto Exchange Posted: 02 Mar 2021 03:51 AM PST I'm going to try to keep this DD short and to the point.

Comparisons in the same sector MARA and RIOT have ~$3.7B market cap at the time of this post. All they do is mine and if you know anything about mining you know they're struggling to turn a profit with the coin price explosion in the last year. They price action of these stocks directly rivals the coins and has become a substitute for playing the coin itself for those who are too lazy to actually buy on an exchange. CAN is a mining equipment supplier with a market cap of $3.5B and yes, all they do is sell the mining rigs, but unlike MARA and RIOT they're actually making money right now. These companies have already exploded and may continue moving alongside the price of BTC, but what if you missed that boat early on and want the next multi-bagger? This is where EBON comes in. They sell ASICs. They sell mining rigs. They mine. They have their own exchange. Their market cap is only $1.16B at the time of this post. My short term price target is $27 which brings their market cap to the $3B range and rivals other these other unidimensional crypto plays. TL;DR Quadruple threat play. Multi-bagger potential. Undervalued compared to peers. Actually making money. Chinese audience. Positions: 1,500 Shares and will continue to add dips as the price action consolidates. As always, do your own DD. I'm not a financial advisor. Please share any knowledge that I may have missed in the comments. Thanks for reading. [link] [comments] |

| Electric Jet-Ski and Snowmobile maker Taiga Motors to go public in merger via Canaccord SPAC CGGZ Posted: 02 Mar 2021 08:40 AM PST Bloomberg reported first about Taiga and CGGZ getting together. The company had their special meeting of shareholders yesterday to approve the transaction and it was approved. Not sure when the actual transaction happens, but it shou ld be relatively soon as there's a big cash infusion coming from CGGZ PIPE. See Bloomberg link for the story: Electric Snowmobile Maker Taiga To Go Public Via Canaccord SPAC [link] [comments] |

| Silver DD Article - Potential rise to $50 Posted: 02 Mar 2021 01:58 PM PST I recently read this article on Seeking Alpha in regards to the global shortage of silver and historical trends predicting a significant rise in price this year. What is everyone's thoughts? It stands up well to my own further DD and I agree with all the points. I see some potential downside but a lot of upside. Of course this is one of those areas where you need to be weary that a fast rise could be followed by a quick drop. A timeframe for this bullish trend is difficult to gauge I would put it within a month or so. The TA on silver at the moment appears medium term bullish if perhaps slightly more consolidation could be expected. Will you be investing in silver? Paper or physical? [link] [comments] |

{kind=link}

| You are subscribed to email updates from Lose money with friends!. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment