Financial Independence Daily FI discussion thread - November 30, 2019 |

- Daily FI discussion thread - November 30, 2019

- We need a major redesign of life -- WashPo

- "Enough"

- Partner wants to own a home. I'm poor. What do?

- Changes to Retirement Plan Following Medical Diagnosis

- Buying a flat in cash or taking mortgage & effect on FIRE target

- Consider diversifying across ETF providers

| Daily FI discussion thread - November 30, 2019 Posted: 30 Nov 2019 12:07 AM PST Please use this thread to have discussions which you don't feel warrant a new post to the sub. While the Rules for posting questions on the basics of personal finance/investing topics are relaxed a little bit here, the rules against memes/spam/self-promotion/excessive rudeness/politics still apply! Have a look at the FAQ for this subreddit before posting to see if your question is frequently asked. Since this post does tend to get busy, consider sorting the comments by "new" (instead of "best" or "top") to see the newest posts. [link] [comments] |

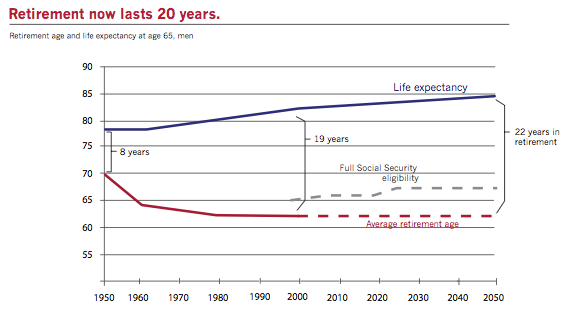

| We need a major redesign of life -- WashPo Posted: 30 Nov 2019 10:47 AM PST Short and interesting read on a Stanford psychologist's opinion on how work culture needs to change. She suggests that our extant life patterns -- go to school until 22, work and retire at 65 -- don't fit elongating life-spans. It's a short piece and just a jumping-off point. But the gist is that the following need to become more common, lest we save our best non-working years for when we're too old to take advantage: mini-retirements, working earlier and getting advanced degrees later, and sharing generational wealth long before death. Interested in thoughts of others on r/financialindependence because the article's suggestion of earlier mini-retirements runs counter (I believe) to the sub's over-arching objective of retiring early and entirely. Any thoughts on whether a higher chance at a 100-year life span affects retirement planning (sooner, repeated, etc)? Consequences of life extension

Earlier and more varied work experience

Earlier sharing of generational wealth

The article again: https://www.washingtonpost.com/opinions/we-need-a-major-redesign-of-life/2019/11/29/a63daab2-1086-11ea-9cd7-a1becbc82f5e_story.html *Edit 1: for grammar *Edit 2: lots of interesting data/trivia on Stanford's Center on Longevity site. For example, trendlines in the age retirees and length of retirement given increasing life expectancies. *Edit 3: This post is now marked as a spoiler, idk what I did. Spoiler might be: you're probably gonna live a couple years longer in retirement and then die. *Edit 4: Removed the quote below from top, because multiple users pointed out that the author is conflating improvements in life expectancy for average human versus those approaching retirement. Life expectancy for men at 65 (Edit 2) increased by at least 7 years but probably not 30:

[link] [comments] |

| Posted: 30 Nov 2019 12:29 PM PST At a party given by a billionaire on Shelter Island, the late Kurt Vonnegut informs his pal, the author Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch 22 over its whole history. Heller responds, "Yes, but I have something he will never have . . . Enough." From John Bogle's speech: https://jamesclear.com/great-speeches/enough-by-john-c-bogle [link] [comments] |

| Partner wants to own a home. I'm poor. What do? Posted: 30 Nov 2019 03:45 PM PST Partner came to me last night with concerns. He wants to own a home. He wants me included but knows I'm poor. Literally, I have no money coming in or in the bank currently and new job doesn't start till Monday. Even with new job, I will not make enough to help him, not that he needs it. He feels it would not be fair to me if he owns the home himself and I pay what I can. That means I'd be paying for a home that technically isn't mine and doesn't have my name on the deed. And if our relationship goes south, I get the boot. There's also a matter that if my name is on the deed, I am responsible for payments as well and if he dies or is unable to pay, it's on me and my $16.50 an hour job. What do you all suggest? Should I nudge him to just get the home or should I just get it with him and contribute whatever I can? [link] [comments] |

| Changes to Retirement Plan Following Medical Diagnosis Posted: 30 Nov 2019 02:19 PM PST I am curious If anyone has made changes to their retirement planning based on a reasonable expectation of a shortened lifespan. I am mid 50s. I would prefer not to get into the details of my illness as I think it is irrelevant. The relevant part is I am mid 50s, married without kids, have about $750K in investments (mostly tax advantages), $90K in more liquid assets and about $300K in home equity. No debt other than $100K left on the mortgage. There are many uncertainties regarding my diagnosis but it is very reasonable that I should be thinking about a life span of 70-75 on the long side and 65 on the short side. At least that is how I am planning. It could actually be shorter, but I am never going to plan around less than a 10 year horizon. I had been planning to work full time until around 58-60, but now that does not seem very palatable. I would love to hear general strategies someone has used to deal with a similar situation. Namely, having time to deal with medical issues and having more free time to enjoy life. Working part time is probably an option and would be good for my mental health, but medical insurance is a concern. My wife is not currently fully employed, but that could change. I am wondering if I should tell my employer or keep it under wraps as well. [link] [comments] |

| Buying a flat in cash or taking mortgage & effect on FIRE target Posted: 30 Nov 2019 01:48 PM PST Let's say I have enough money to buy a flat where I want to live in cash. Or I can take mortgage and invest it in stock market. If this goes well I can get to my FIRE target much sooner or much later if it goes bad. I can take mortgage for 0.7% interest and have 0% on capital gains if held over 1Y. Given the current valuations would you in my situations take the mortgage? Maybe half cash and half mortgage? Would you invest the cash by monthly averaging over 1 year, 2 years, something else? I am based in Europe, country with €, would be buying US stock ETFs. Thank you for your opinion and/or questions. Edit: it's 30Y mortgage, 0.7% interest fixed for 3Y, afterwards according to market rates [link] [comments] |

| Consider diversifying across ETF providers Posted: 30 Nov 2019 03:59 AM PST I recently heard a story from a friend of mine that something happened to one of their ETFs and they were forced to pay capital gain tax for that position. I decided to estimate how bad the impact of such an event can be when saving for FIRE. Let's imagine that you invest in one ETF (e.g. world ETF). Obviously the impact depends on what portion of your stash is unrealized capital gains. I did some calculations (spreadsheet) and got (at a time when one reaches FI)

In other words, if you have 30% saving rate & your FI number is 100k USD, at a time your pre-tax networth reaches 100k USD, 66k of these are untaxed capital gains. Let's say that one is very unlucky and exactly when they reach their FI number, their ETF is liquidated and they are forced to pay all capital gains. Assuming 26.375% capital gain tax (i.e. Germany), this will set them back by 2.9%, 10.5% or 17.4% based on their savings rate (90%, 60%, 30% respectively). Following my example above, this means paying 17.4k USD taxes and having 83.6k USD left. In order to reach 100k again with 30% savings rate, they will need to work 20 more months. ETF liquidation is only one example of such an event, there can also be fund structure or ISIN change. [link] [comments] |

{kind=link}

| You are subscribed to email updates from financial independence / early retirement. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment