Good afternoon and happy Saturday to all of you here on r/StockMarket. I hope everyone on this subreddit made out pretty nicely in the market this past week, and is ready for the new trading week ahead.

Here is everything you need to know to get you ready for the trading week beginning July 1st, 2019.

What to watch in markets for the week ahead: After G-20, focus shifts to jobs report - (Source)

The monthly jobs number is always important but this time, it could be even bigger news, since it may actually help tell us how much the Fed will cut interest rates this summer.

The report won't be the only bit of data the Fed will look at before it meets July 30-31, but it could show whether the economy has hit a weak enough streak in hiring that the Fed will want to act.

Economists expect that 158,000 jobs were created in June, up sharply from the disappointing 75,000 in May, according to Refinitiv. The unemployment rate is expected to remain unchanged at 3.6% and average hourly earnings are expected to rise by 0.3%.

"It's going to be better than last month. Otherwise, we've got a problem," said Joseph LaVorgna, chief economist at Natixis Americas. "We're saying it's something like 130,000. If it's weak, the markets are going to assume the Fed's going 50 [basis points]. If you have a number in June, like you had in May, they would go 50."

After the weekend's G-20 headlines, the jobs report is the big focus for markets in the coming week, along with OPEC's two-day meeting Monday and Tuesday. OPEC is widely expected to extend 1.2 million barrels a day in production cuts in a deal with Russia, and oil isn't expected to react much, unless there's a surprise.

Markets also kick off the third quarter in the holiday-shortened Fourth of July week, after one of the best first halves in more than 20 years for stocks.

The jobs report follows some other important data in the coming week, and comes as the slowing in the economy is taking a worrisome turn and beginning to hit some of the consumer-related data. A lagging indicator, the jobs data may provide some guidance on the well-being of consumers, which drive about 70% of the U.S. economy.

Both consumer confidence and consumer sentiment readings in June were weaker amid concerns about trade. Consumer spending increased just 0.2% in May, leading some economists on Friday to slash their expectations for both consumption in the second quarter and second quarter economic growth. J.P. Morgan economists trimmed their second quarter GDP forecast to 1.5% from 1.9%

The economy now exits the second quarter, and first half of the year, with some big doubts hanging over the outlook. That makes some of the data in the coming week, the first week of the third quarter, even more relevant. For instance, ISM manufacturing and PMI manufacturing data are released Monday. Both are important to the outlook or the manufacturing sector, which has been weak. Car sales are released Tuesday, and they will also be an important look into manufacturing and the consumer.

"If the jobs number is good but let's say the CPI and retail sales data turns out to be a lot softer, or GDP revised meaningfully down, it's not just employment. The possibility of the Fed doing more than 25 [basis points] does not end with the employment report," LaVorgna said.

The May jobs report was an important turning point for markets, changing the minority view of some economists that the Fed could cut interest rates into a consensus expectation. But that consensus has not settled on when and how much the Fed will chop rate.

The Fed signaled after its June meeting that it was leaning toward a cut, exiting its neutral posture, and that it could act soon if it had to.

So the jobs report, "is important for better or worse. The market's been bullying the Fed for the last couple of decades and if anything, it's gotten even more powerful. If it's weak, the market is going to push them to do more, but the Fed will be fearful of disappointing the market. They'll also be fearful the economy is weak against the backdrop of trade uncertainty," said LaVorgna.

At this point, fed funds futures are pricing in a full quarter-point rate cut for the July meeting and a portion of a second cut. Economists mostly expect two cuts this year, whether starting in July or September, with another likely by either September or December.

This past week saw the following moves in the S&P:

Major Indices for this past week:

Major Futures Markets as of Friday's close:

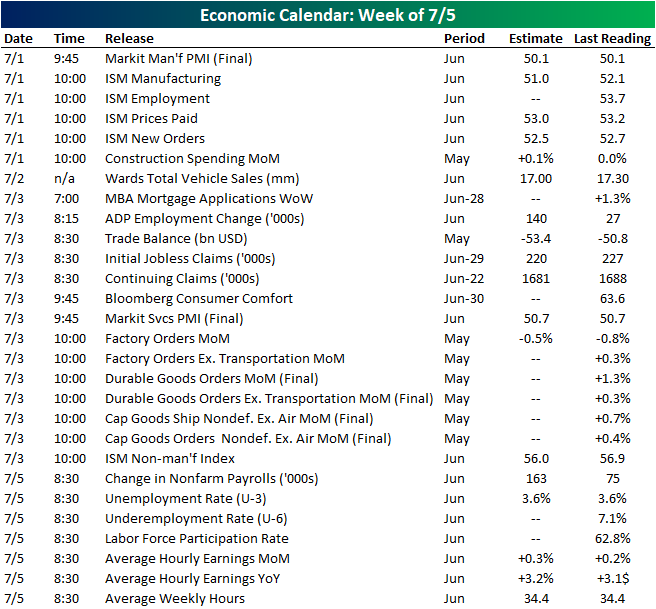

Economic Calendar for the Week Ahead:

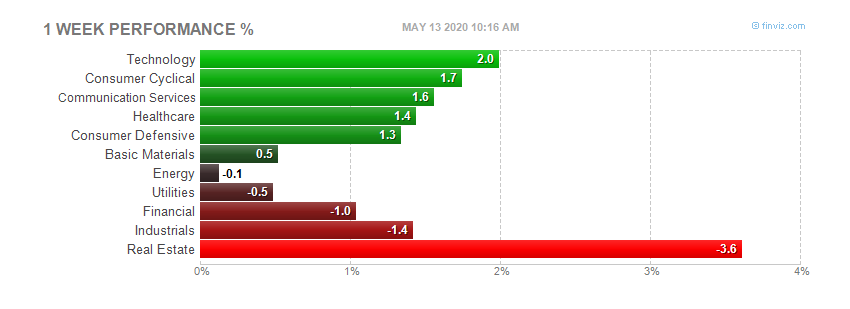

Sector Performance WTD, MTD, YTD:

Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:

S&P Sectors for the Past Week:

Major Indices Pullback/Correction Levels as of Friday's close:

Major Indices Rally Levels as of Friday's close:

Most Anticipated Earnings Releases for next month:

Here are the upcoming IPO's for this week:

([CLICK HERE FOR THE CHART!]())

NONE.

Friday's Stock Analyst Upgrades & Downgrades:

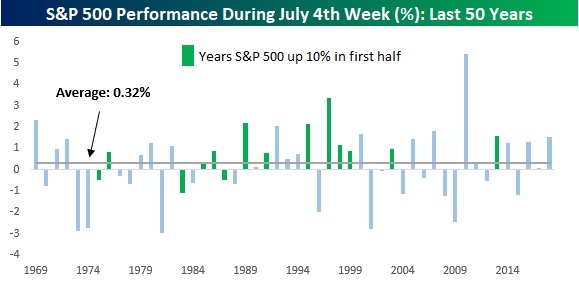

July 4th Market Returns

With the first half winding down to a close, Summer is in full swing as July 4th quickly approaches. While the days leading up to or after July 4th are usually on the quiet side with many people taking vacations, for the stock market, it is usually a relatively positive week. The chart below shows the S&P 500's performance during the July 4th week measuring performance from the Friday before July 4th until the Friday after. In years where July 4th falls on a Friday or Saturday, we measure the S&P 500's performance in the week leading up to July 4th.

For the July 4th week, going back to 1969, the S&P 500 has seen an average gain of 0.32% with positive returns 60% of the time. In the charts below, we have also included green shading in years where the S&P 500 was up 10%+ in the first half (as it is this year). In those years, returns during the July 4th week have been much better with an average gain of 0.93% and positive returns 79% of the time. In fact, the last time the S&P 500 was down during the July 4th week in a year where the S&P 500 was up 10%+ in the first half was in 1986!

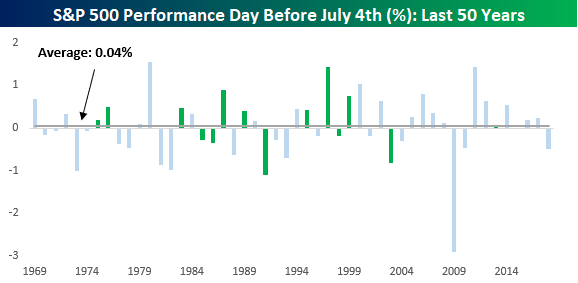

Similar to the July 4th week, the day before July 4th has also historically been positive but not nearly to the same degree. On those days, the S&P 500 has averaged a gain of 0.04% with positive returns only slightly more than half of the time (54%). In years where the S&P 500 was up over 10% in the first half, the day before July 4th is considerably better, averaging a gain of 0.17% with gains 64% of the time.

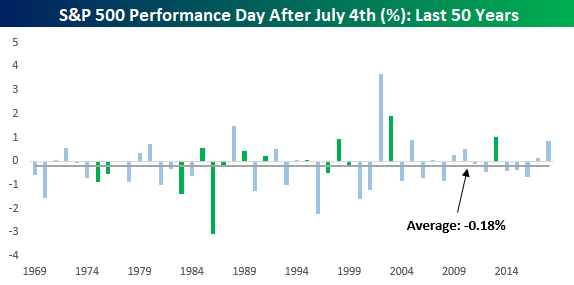

With people out celebrating the July 4th holiday, the hangover sets in after. As shown below, the average S&P 500 change on the trading day after July 4th is a decline of 0.18% with gains only 42% of the time. In years when the S&P 500 was up over 10% in the first half, the declines aren't as bad, but at -0.12% and gains only half of the time, they aren't positive either. This year the day after July 4th will also feature the June Non-Farm Payrolls report. That will be fun!

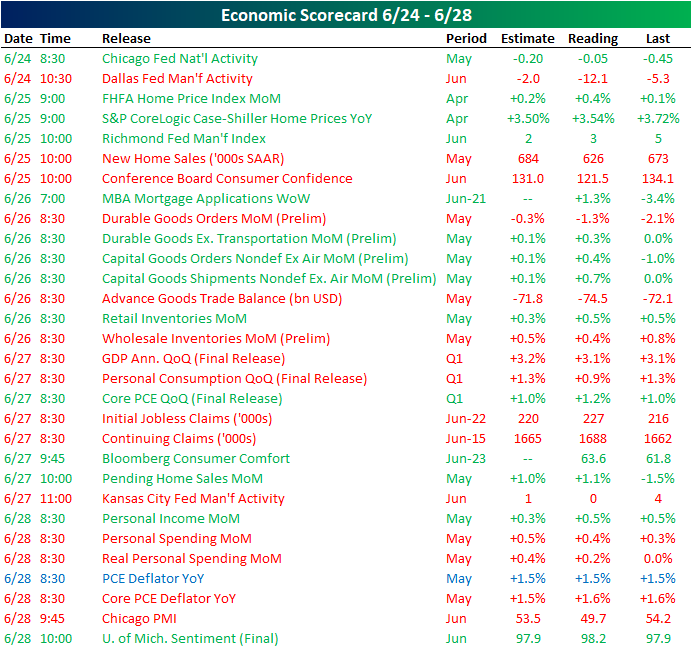

Next Week's Economic Indicators - 6/28/19

In posts yesterday and Monday, we made note of the increasingly disappointing economic data out of the US relative to expectations so far in 2019. This week's data only added to the woes as the Citi Economic Surprise Index for the US now sits only 0.73% above its April low.

Over half of this week's releases came in worse than the prior period of estimates. The Chicago Fed's National Activity Index was the first release this week showing improvements from the April data and coming in above estimates, but the indicator is still showing contracting activity (reading below zero). The Dallas Fed's Manufacturing Activity index also was out on Monday showing far weaker results. Later in the week, on Thursday, the Kansas City Fed released their own manufacturing activity index completing our Five Fed Composite which is painting a bleak picture for the manufacturing sector. There was also a good amount of housing data this week with overall solid results including stronger than expected home prices (via the FHFA index and S&P CoreLogic's Case-Shiller Index) but disappointing new home sales on Tuesday, improved MBA Mortgage Applications on Wednesday, and a much better Pending Home Sales print on Thursday. Chicago PMI dropped below 50 on Friday, which is a sign of contraction, but Michigan Confidence beat estimates. One other major release this week was the third and final release of quarterly GDP, which held steady at 3.1% QoQ but was below estimates of an increase to 3.2%.

Despite a shortened week due to the July 4th holiday, next week is set up to be a busy one. On Monday, Markit will release their final June PMI on manufacturing alongside the ISM reading later that morning. While Markit measures on manufacturing are expected to hold steady at 50.1, ISM data is anticipated to fall 1.1 down to 51. The only release Tuesday will be data on vehicle sales, which are expected to fall to 17 mm SAAR. On Thursday, there will be no releases and US markets will be shuttered in observance of the July 4th holiday. Additionally, markets will close early (1:00 PM EST) on Wednesday. In spite of this shortened session and day off, there is a huge slug of data to be released Wednesday. Following up the manufacturing PMIs, Markit and ISM non-manufacturing indicators are all due out on Wednesday. In the late morning, final May data on Factory, Durable, and Capital Goods Orders are also going to be released. Alongside the standard Wednesday release of MBA Mortgage Applications, other weekly data that is typically released on Thursday will be pushed ahead one day including Initial Jobless Claims and Bloomberg Consumer Comfort. ADP employment numbers are expected to show improvements when it releases on Wednesday ahead of Friday's Nonfarm payrolls report, which is also forecasting a solid improvement from the previous month.

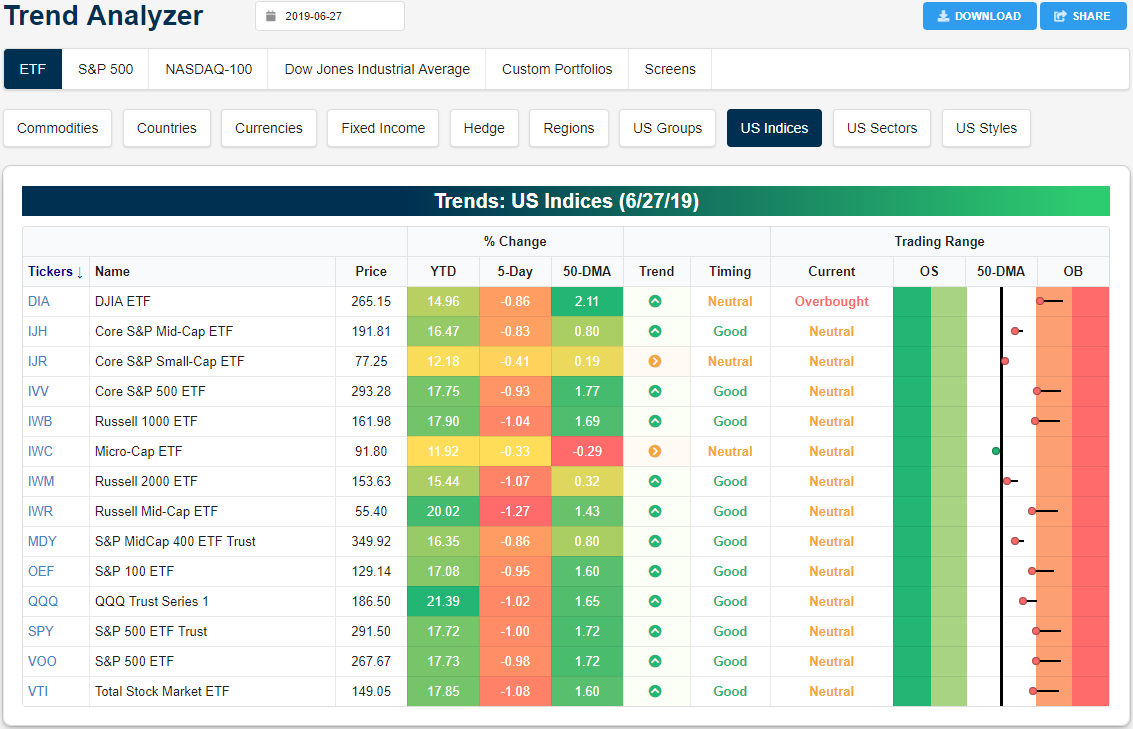

Trend Analyzer - 6/28/19 - Teetering On Overbought

After the S&P 500 (SPY) set a new all-time high last Thursday, stocks have yet to make a push back above these levels as all of the major index ETFs sit below where they were at last Thursday's close. This pullback was partially a function of the large-cap major index ETFs like the Russell 1000 (IWB) working off overbought levels. Whereas all of these were overbought last week, currently only the Dow (DIA) still sits in overbought territory although other large caps are teetering on joining DIA. The Core S&P Small Cap (IJR) and Micro Cap (IWC) are only lower by 0.41% and 0.33%, respectively. These are smaller losses compared to other ETFs which lost around 1%. Ironically, this outperformance also comes as IJR and IWC are now showing sideways trends rather uptrends across the rest of the ETFs. Granted, not all small-cap indices have been outperforming. Another small-cap index, the Russell 2000 (IWM), has seen performance more inline with other ETFs, declining 1.07%.

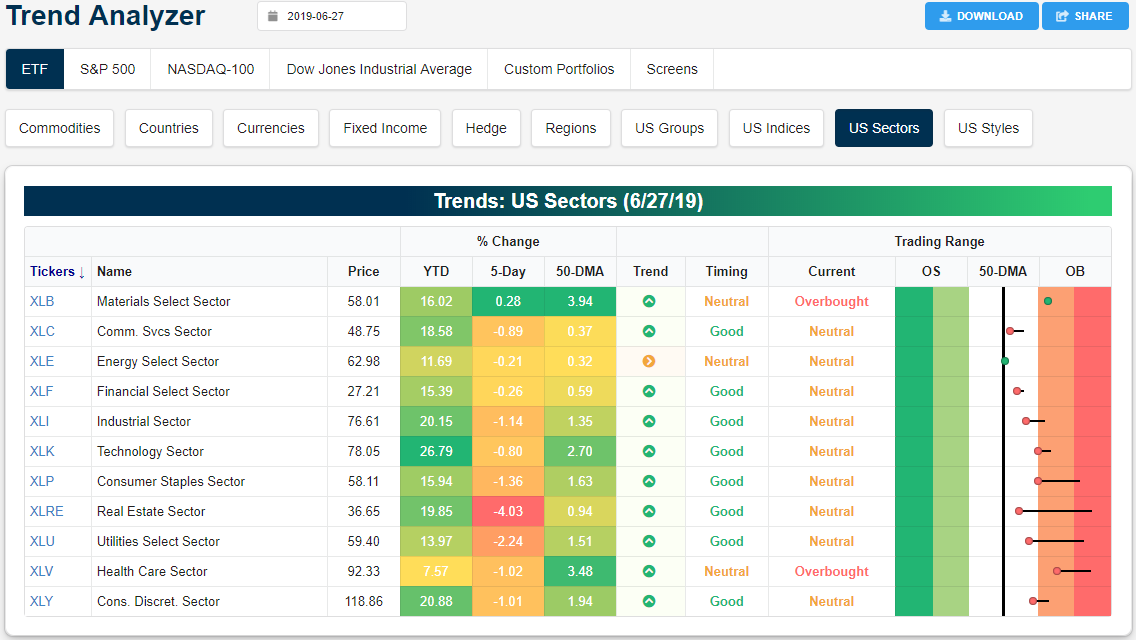

Every sector except Materials (XLB) is lower over the last week. As shown in our Trend Analyzersnapshot below, it's the defensives that are finally lagging, with Real Estate (XLRE) down 4% and Utilities (XLU) down 2% since last Thursday's close. At the moment, only Materials and Health Care are overbought, while the rest are neutral.

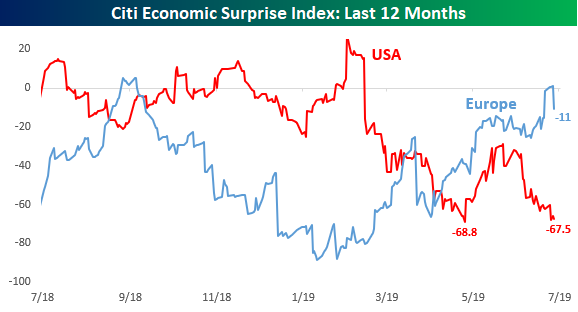

US Falls to the Bottom of the Pack

In a post earlier this week, we provided an update to the Citi Economic Surprise indices broken out by region. With economic data in the US continuing to disappoint this week, the Citi Surprise index (percentage of economic indicators that are beating vs. missing estimates) for the US is coming increasingly close to taking out its late April low and declining to its lowest levels in two years. What's also notable about the current reading is that at the most recent reading of -67.5, the surprise index for the US is more negative than any other country or region that this series tracks.

Below we compare the Citi surprise reading for the US and Europe over the last twelve months, and what a reversal it has been. Heading into 2019, economic data in the US was coming in much better relative to expectations versus Europe, but ever since then, data in the US has been getting progressively worse relative to expectations, while data in Europe has been consistently improving.

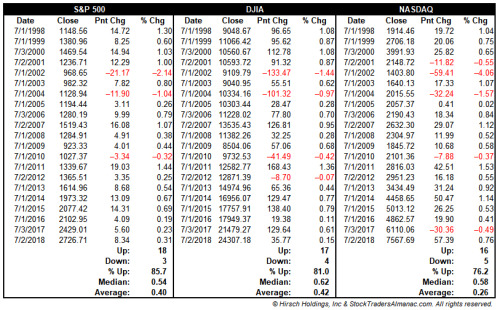

July's First Trading Day—Most Bullish Day, S&P 500 has Advanced 85.7% of the Time

July's first trading day is the best performing first trading day of all twelve months with DJIA gaining a cumulative 1,175.74 points since 1998. Over the past 21 years, DJIA's first trading day of July has produced gains 81.0% of the time with an average gain of 0.40%. S&P 500 has advanced 85.7% of the time (average gain 0.42%). NASDAQ has been slightly weaker at 76.2% (0.26% average gain). No other day of the year exhibits this amount of across-the-board strength which makes a solid case for declaring the first trading day of July the most bullish day of the year over the past 21 years.

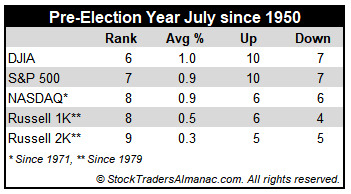

Pre-Election Year July Performance Mixed

July historically is the best performing month of the third quarter however, the mostly negative results in August and September make the comparison easy. Two "hot" Julys in 2009 and 2010 where DJIA and S&P 500 both gained greater than 6% and a strong performance in 2013 have boosted July's average gains since 1950 to 1.2% and 1.1% respectively. Such strength inevitability stirs talk of a "summer rally", but beware the hype, as it has historically been the weakest rally of all seasons (page 74, Stock Trader's Almanac 2019).

July begins NASDAQ's worst four months and is the third weakest performing NASDAQ month since 1971, posting a 0.5% average gain. Dynamic trading often accompanies the first full month of summer as the beginning of the second half of the year brings an inflow of new capital. This creates a bullish beginning, a soft week after options expiration and strength towards the end.

Pre-election-year July rankings are something of a mixed bag, ranking #6 for DJIA and #7 S&P 500, averaging gains of 1.0% and 0.9% respectively (since 1950); while NASDAQ (since 1971) and Russell 1000 (since 1979) pre-election Julys both rank #8. NASDAQ has only advanced in six of the last twelve pre-election Julys. Russell 2000 has advanced in five of its last ten. Despite tech's and small-cap's meager pre-election July track record, NASDAQ and Russell 2000 have averaged gains of 0.9% and 0.3% respectively.

STOCK MARKET VIDEO: Stock Market Analysis Video for June 28th, 2019

STOCK MARKET VIDEO: ShadowTrader Video Weekly 06.30.19

Here are the most notable companies (tickers) reporting earnings in this upcoming trading month ahead-

- $NFLX

- $BA

- $F

- $UNH

- $INTC

- $T

- $CLF

- $BAC

- $PEP

- $GOOGL

- $AEMD

- $DAL

- $JPM

- $C

- $SMPL

- $HAL

- $WFC

- $IRBT

- $AYI

- $JNJ

- $MMM

- $BBBY

- $YRD

- $NOK

- $ISCA

- $CAT

- $CMG

- $ISRG

- $KO

- $MA

- $LEVI

- $BMY

- $SLB

- $INFY

- $OMN

- $GS

- $CSX

- $PGR

- $UPS

- $ERIC

- $ABT

- $AA

- $CNC

Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

Monday 7.1.19 Before Market Open:

Monday 7.1.19 After Market Close:

Tuesday 7.2.19 Before Market Open:

Tuesday 7.2.19 After Market Close:

([CLICK HERE FOR TUESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

NONE.

Wednesday 7.3.19 Before Market Open:

Wednesday 7.3.19 After Market Close:

([CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

NONE.

Thursday 7.4.19 Before Market Open:

([CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!]())

NONE. (U.S. MARKETS CLOSED IN OBSERVANCE OF THE 4TH OF JULY HOLIDAY.)

Thursday 7.4.19 After Market Close:

([CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

NONE. (U.S. MARKETS CLOSED IN OBSERVANCE OF THE 4TH OF JULY HOLIDAY.)

Friday 7.5.19 Before Market Open:

Friday 7.5.19 After Market Close:

([CLICK HERE FOR FRIDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

NONE.

Kraft Heinz Company $31.04

Kraft Heinz Company (KHC) is expected to report earnings at approximately 5:00 PM ET on Wednesday, July 31, 2019. The consensus earnings estimate is $0.60 per share on revenue of $6.08 billion and the Earnings Whisper ® number is $0.62 per share. Investor sentiment going into the company's earnings release has 37% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 32.58% with revenue decreasing by 3.55%. Short interest has increased by 41.8% since the company's last earnings release while the stock has drifted lower by 13.4% from its open following the earnings release to be 26.4% below its 200 day moving average of $42.17. Overall earnings estimates have been revised lower since the company's last earnings release. On Wednesday, May 29, 2019 there was some notable buying of 4,513 contracts of the $22.50 put expiring on Friday, August 16, 2019. The stock has averaged a 10.0% move on earnings in recent quarters.

Tesla, Inc. $223.46

Tesla, Inc. (TSLA) is expected to report earnings at approximately 5:15 PM ET on Wednesday, July 24, 2019. The consensus estimate is for a loss of $1.55 per share on revenue of $6.78 billion. Investor sentiment going into the company's earnings release has 29% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 54.68% with revenue increasing by 69.41%. Short interest has increased by 33.3% since the company's last earnings release while the stock has drifted lower by 12.4% from its open following the earnings release to be 21.5% below its 200 day moving average of $284.79. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 7.4% move on earnings in recent quarters.

Amazon.com, Inc. -

Amazon.com, Inc. (AMZN) is expected to report earnings at approximately 4:00 PM ET on Thursday, July 25, 2019. The consensus earnings estimate is $5.28 per share on revenue of $62.51 billion. Investor sentiment going into the company's earnings release has 77% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 4.14% with revenue increasing by 18.20%. Short interest has increased by 20.2% since the company's last earnings release while the stock has drifted lower by 1.8% from its open following the earnings release to be 9.0% above its 200 day moving average of $1,737.01. Overall earnings estimates have been revised lower since the company's last earnings release. The stock has averaged a 4.0% move on earnings in recent quarters.

Advanced Micro Devices, Inc. $30.37

Advanced Micro Devices, Inc. (AMD) is expected to report earnings at approximately 4:20 PM ET on Tuesday, July 30, 2019. The consensus earnings estimate is $0.05 per share on revenue of $1.52 billion. Investor sentiment going into the company's earnings release has 75% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 66.67% with revenue decreasing by 13.44%. Short interest has decreased by 1.3% since the company's last earnings release while the stock has drifted higher by 4.9% from its open following the earnings release to be 21.1% above its 200 day moving average of $25.07. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 12.2% move on earnings in recent quarters.

Facebook Inc. $193.00

Facebook Inc. (FB) is expected to report earnings at approximately 4:05 PM ET on Wednesday, July 24, 2019. The consensus earnings estimate is $1.90 per share on revenue of $16.40 billion. Investor sentiment going into the company's earnings release has 88% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 9.20% with revenue increasing by 23.95%. Short interest has increased by 10.3% since the company's last earnings release while the stock has drifted lower by 2.0% from its open following the earnings release to be 19.5% above its 200 day moving average of $161.50. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 8.6% move on earnings in recent quarters.

Netflix, Inc. $367.32

Netflix, Inc. (NFLX) is confirmed to report earnings at approximately 4:00 PM ET on Wednesday, July 17, 2019. The consensus earnings estimate is $0.56 per share on revenue of $4.93 billion. Investor sentiment going into the company's earnings release has 65% expecting an earnings beat The company's guidance was for earnings of approximately $0.55 per share. Consensus estimates are for earnings to decline year-over-year by 34.12% with revenue increasing by 26.18%. Short interest has increased by 16.4% since the company's last earnings release while the stock has drifted higher by 0.6% from its open following the earnings release to be 9.3% above its 200 day moving average of $335.96. Overall earnings estimates have been revised lower since the company's last earnings release. On Thursday, June 27, 2019 there was some notable buying of 752 contracts of the $305.00 put expiring on Friday, October 18, 2019. The stock has averaged a 5.8% move on earnings in recent quarters.

Apple, Inc. $197.92

Apple, Inc. (AAPL) is expected to report earnings at approximately 4:30 PM ET on Tuesday, July 30, 2019. The consensus earnings estimate is $2.12 per share on revenue of $53.47 billion. Investor sentiment going into the company's earnings release has 62% expecting an earnings beat The company's guidance was for earnings of $1.93 to $2.18 per share. Consensus estimates are for earnings to decline year-over-year by 9.40% with revenue increasing by 0.38%. Short interest has decreased by 16.0% since the company's last earnings release while the stock has drifted lower by 5.7% from its open following the earnings release to be 5.0% above its 200 day moving average of $188.48. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 5.5% move on earnings in recent quarters.

Microsoft Corp. $133.96

Microsoft Corp. (MSFT) is expected to report earnings at approximately 4:05 PM ET on Wednesday, July 24, 2019. The consensus earnings estimate is $1.21 per share on revenue of $32.63 billion. Investor sentiment going into the company's earnings release has 80% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 7.08% with revenue increasing by 8.46%. Short interest has decreased by 2.5% since the company's last earnings release while the stock has drifted higher by 3.0% from its open following the earnings release to be 17.4% above its 200 day moving average of $114.09. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 2.5% move on earnings in recent quarters.

Boeing Co. $364.01

Boeing Co. (BA) is confirmed to report earnings at approximately 7:30 AM ET on Wednesday, July 24, 2019. The consensus earnings estimate is $1.81 per share on revenue of $21.57 billion. Investor sentiment going into the company's earnings release has 34% expecting an earnings beat. Consensus estimates are for earnings to decline year-over-year by 45.65% with revenue decreasing by 11.08%. Short interest has increased by 10.9% since the company's last earnings release while the stock has drifted lower by 3.7% from its open following the earnings release to be 0.2% above its 200 day moving average of $363.22. Overall earnings estimates have been revised lower since the company's last earnings release. The stock has averaged a 3.0% move on earnings in recent quarters.

Ford Motor Company $10.23

Ford Motor Company (F) is confirmed to report earnings at approximately 4:15 PM ET on Wednesday, July 24, 2019. The consensus earnings estimate is $0.33 per share on revenue of $35.73 billion. Investor sentiment going into the company's earnings release has 90% expecting an earnings beat. Consensus estimates are for year-over-year earnings growth of 22.22% with revenue decreasing by 8.20%. Short interest has increased by 4.8% since the company's last earnings release while the stock has drifted higher by 2.0% from its open following the earnings release to be 10.1% above its 200 day moving average of $9.29. Overall earnings estimates have been revised higher since the company's last earnings release. The stock has averaged a 6.1% move on earnings in recent quarters.

DISCUSS!

What are you all watching for in this upcoming holiday-shortened week ahead?

I hope you all have a fantastic weekend and a great trading week. Happy (early) 4th of July r/StockMarket!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[link]](https://i.redd.it/f81b8qrqpa731.png){kind=link}

No comments:

Post a Comment